Weekly update #136

The latest news on the fintech and VC ecosystems

Welcome to this edition of the weekly newsletter. The idea behind this is to gather all the information in the startup ecosystem in one place, with a special focus on the fintech market and the VC industry.

The latest episode of Builders has been released this week! In this episode, I sit down with Sander Janca-Jensen, CEO and co-founder of Flatpay. You can watch the full episode here on YouTube, or listen to it here on Spotify or here on Apple Podcast. But take a look at a quick clip first:

Sander is the CEO and cofounder of Flatpay, the Danish fintech company building payments, point of sale and financial services for small and medium sized physical merchants, including restaurants, cafés and independent shops.

Founded in 2022, Flatpay has quickly become one of Denmark’s fastest growing fintech scaleups, reaching unicorn status after a €145 million funding round that valued the company at around €1.5 billion, up from roughly $100 million in 2024.

Before launching the company, he spent almost six years at Verisure, where he held senior roles including Deputy Managing Director and Field Sales Director, managing more than 450 salespeople and overseeing around DKK 300 million in annual profit and loss responsibility. Earlier in his career, he held multiple sales leadership roles at Berlingske Media and cofounded SimplyJob, which reached more than 125,000 users within one year before its exit in 2018.

With him, we will talk about the importance of physical sales in payments, hiring in fast growing environments, and the fintech trends in the payment space in Europe.

Coming back to us, I’ve been reading a very interesting report this week, the “ Behind Stablecoins: The emerging architecture of on-chain money” from McKinsey & Company. The content highlights how in 2025, the stablecoin market supported approximately $400 billion in organic payment activity. This volume is a minute proportion of the several quadrillion dollars that move annually through global payment systems. However, in parts of Asia, digital-asset ecosystems and progressive regulatory frameworks are already driving significant institutional volume. What is missing for stablecoin to become a pillar of the financial markets? Here my main takeaways:

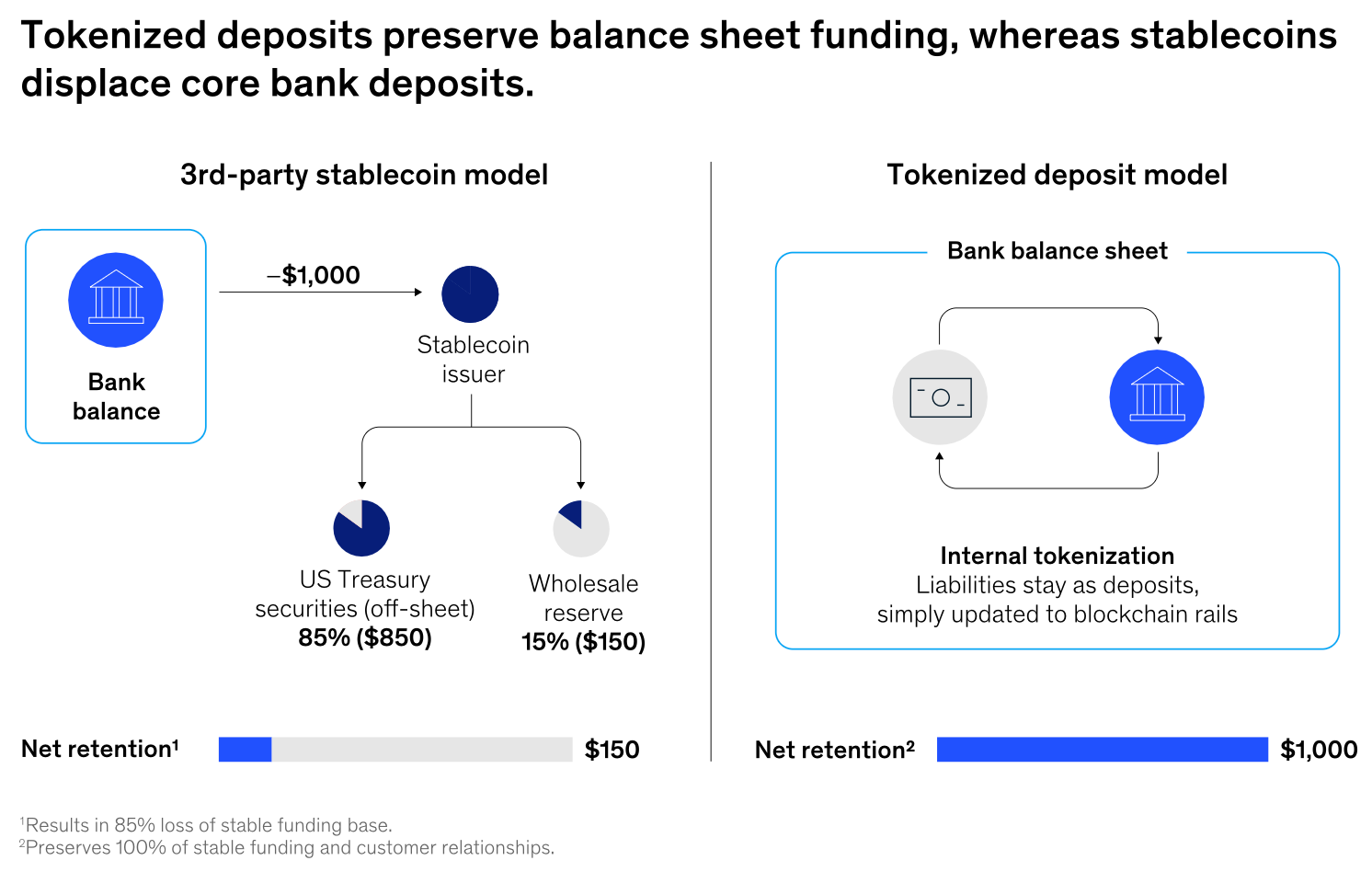

Stablecoins and tokenized deposits differ mainly in how they affect bank balance sheets. Third party stablecoins, issued by companies such as Circle and Tether, can move funding away from banks by converting retail deposits into tokenized liabilities. In many cases, only about 15% of each $1,000 converted returns to the banking system as wholesale reserves, while the remaining 85% is typically invested in assets such as US Treasuries.

Tokenized deposits, by contrast, allow banks to modernize their own liabilities without losing balance sheet funding. They can offer programmability, faster settlement, and greater operational efficiency while preserving the customer relationship.

For banks, the main risk is not just deposit leakage, but losing control of the transaction relationship to third party digital rails. This could pressure funding models, net interest margins, and liquidity coverage ratios, prompting banks to develop their own digital deposit alternatives.

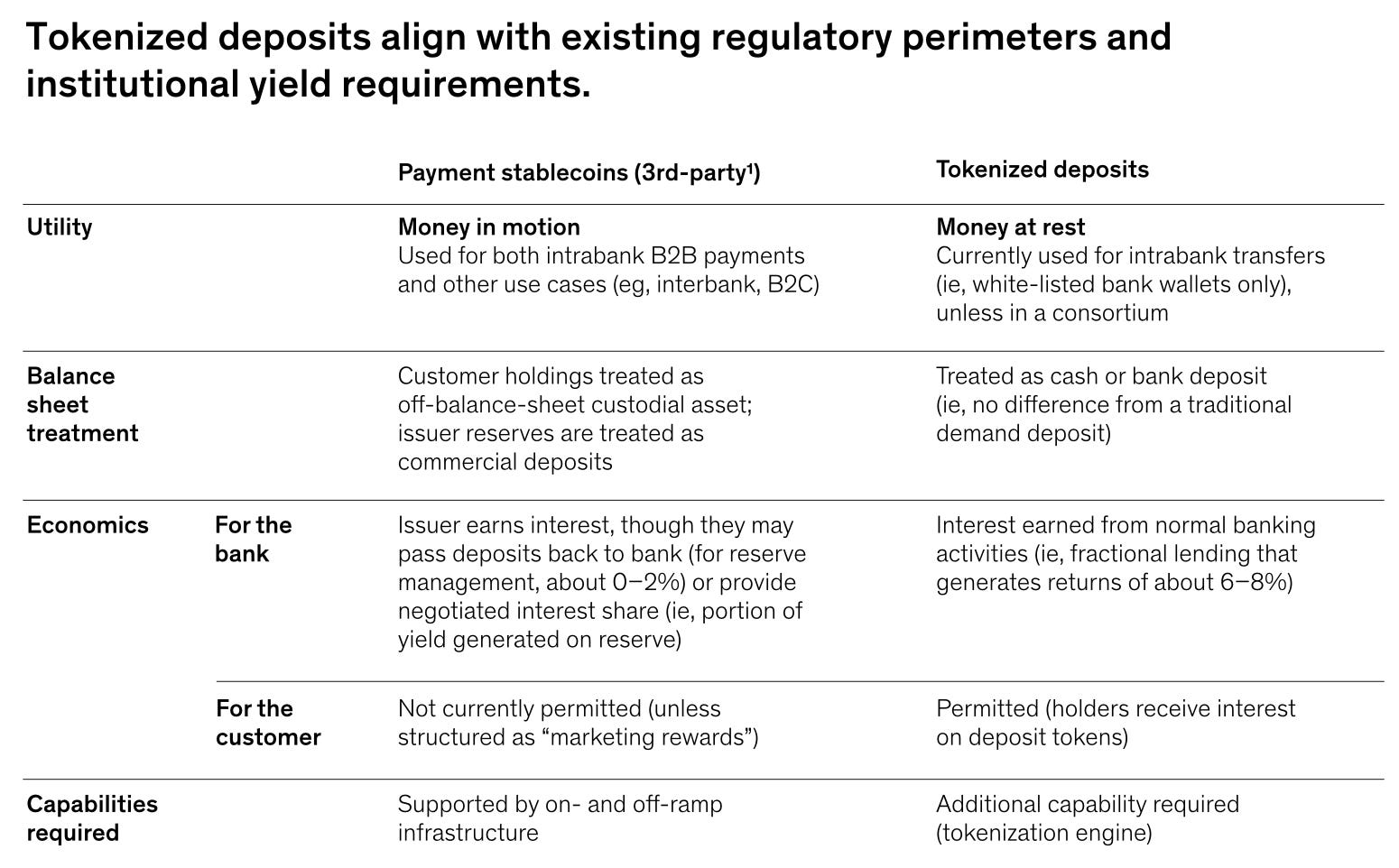

Banks retain an advantage in balance sheet management, but third party stablecoins currently lead in liquidity, accessibility, and network effects. Major stablecoins such as Circle ’s USDC and Tether.io ’s USDT are widely integrated across digital asset markets and supported by deep liquidity on exchanges including Coinbase, Binance, and OKX. This makes them useful for low cost foreign exchange and fast settlement in certain crypto native corridors.

Tokenized deposits remain more fragmented. They are often issued on proprietary, permissioned blockchains, which limits cross bank exchange and fungibility. A tokenized dollar from one bank is not easily interchangeable with one from another, recreating the fragmentation blockchain aims to solve. The main barrier is interoperability. If global banking coalitions can address this in 2026, near instant payments using commercial bank money could become viable.

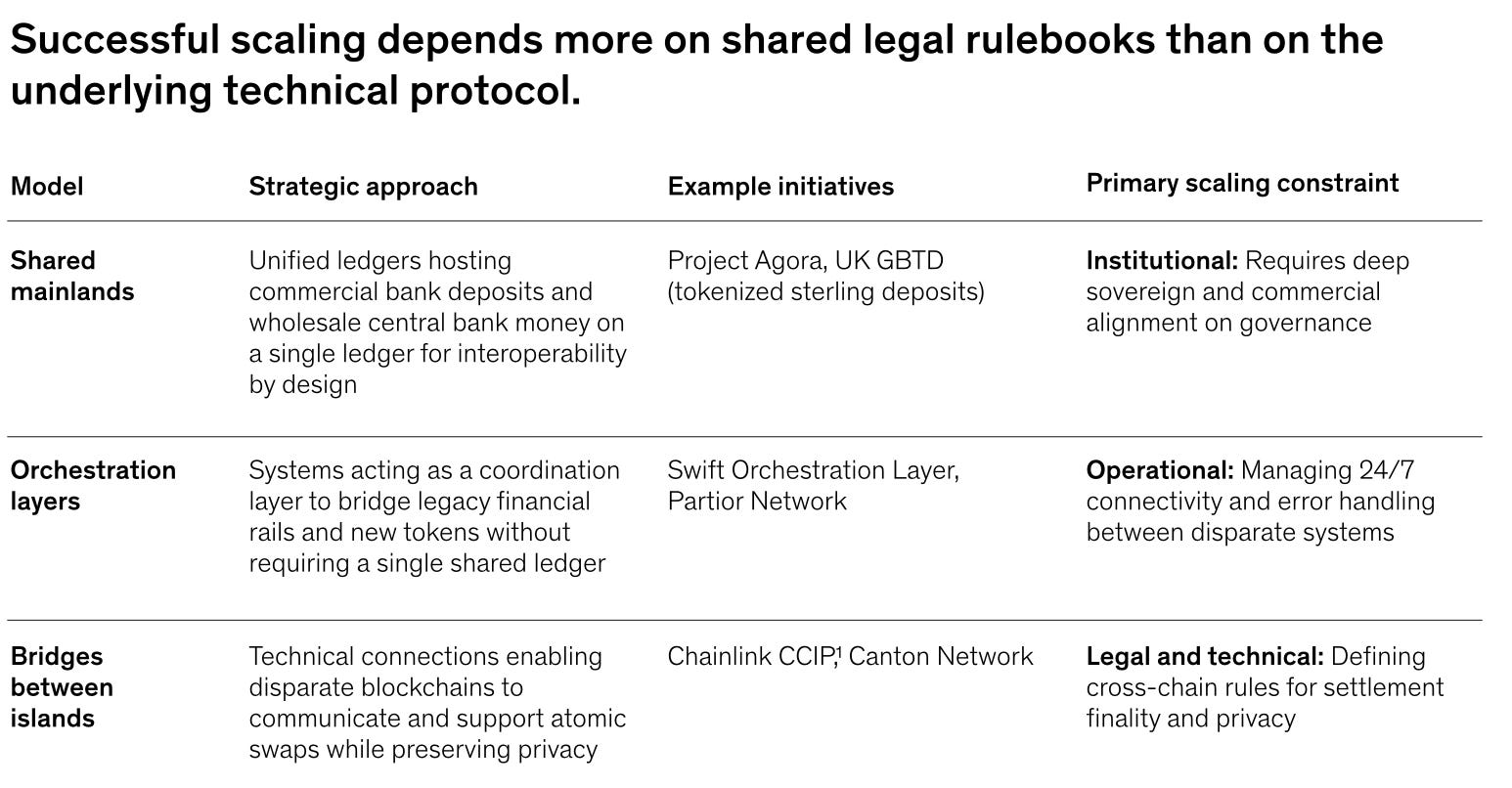

Tokenized deposits can scale only if banks solve the fragmentation created by proprietary blockchains. Progress is not purely technical. Banks also need common rules on legal finality, liability, and operating standards, which are often the slowest parts of financial innovation.

Three interoperability models are emerging. The first is shared ledgers, where commercial bank deposits and wholesale central bank money operate on the same infrastructure. Examples include the BIS’s Project Agora and the UK’s tokenized sterling deposits initiative.

The second is orchestration layers, which connect tokenized assets with existing payment systems without requiring one shared ledger. Swift and Partior are examples of this approach.

The third is blockchain bridges, which allow different networks to communicate while preserving privacy. Chainlink’s work with Swift and the Canton Network show how this model could support simultaneous exchange across diverse systems

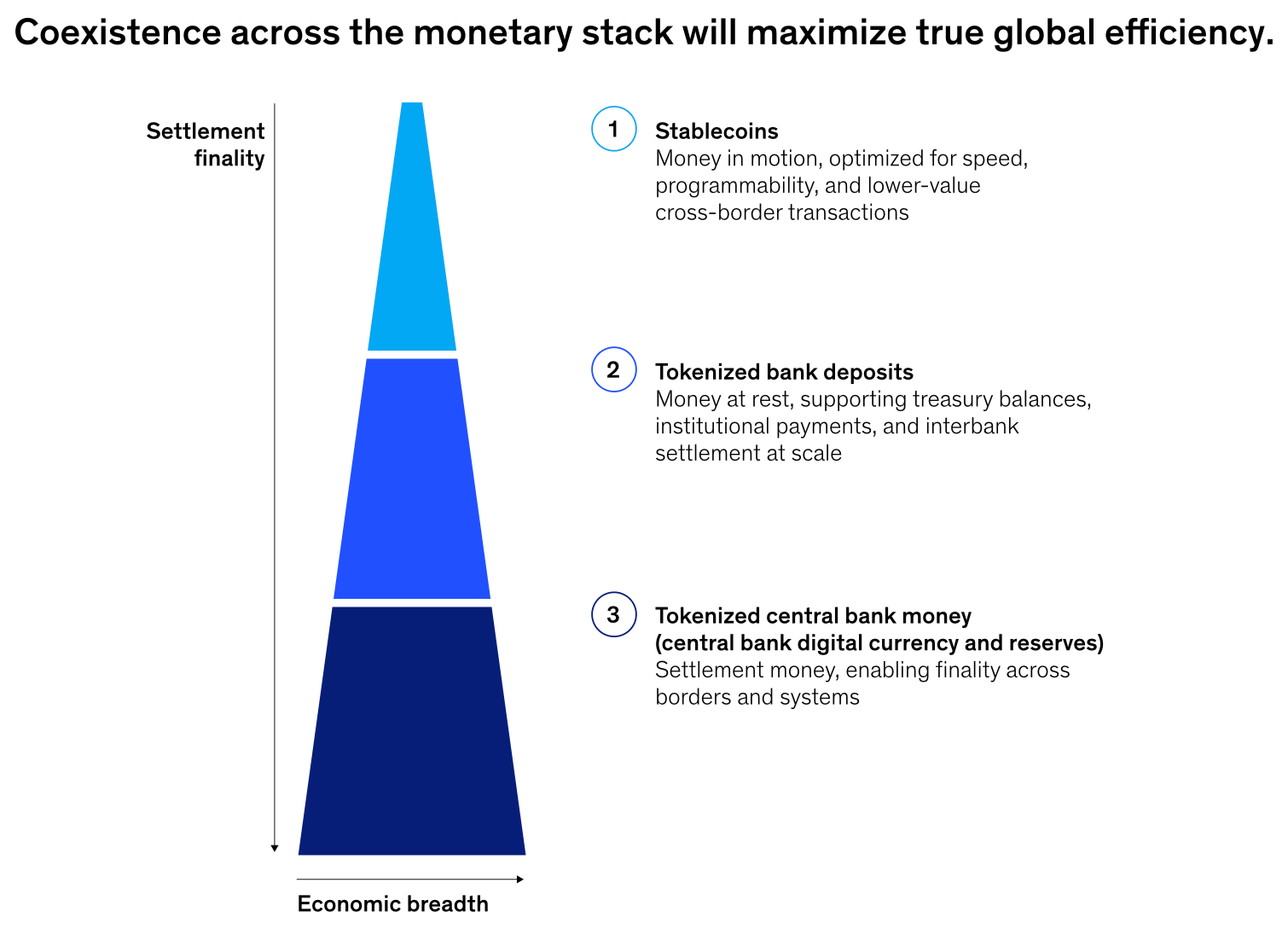

2026 could become a decisive year for on-chain money, as consortiums and interoperability projects test which models can reduce friction in global payments. The future is unlikely to rely on a single digital asset. Instead, different forms of tokenized value may coexist in a layered system.

Stablecoins are likely to serve as “money in motion,” supporting fast, lower value cross border payments and automated disbursements, especially where traditional banking access is limited.

Tokenized bank deposits could function as “money at rest,” supporting treasury balances, institutional payments, and interbank settlement. While tokenized central bank digital currencies may become “settlement money,” providing finality and reducing counterparty risk between systems. The success of on chain money will depend less on one dominant asset and more on how these layers interoperate.

But let’s take a closer look at the main news of the last seven days. Bending Spoons file for an IPO at Nasdaq, Revolut weighs secondary shares sale at $115B valuation, Boursorama integrates Wero in France and Kraken became FIFA crypto sponsor for the world cup. But also, Intesa Sanpaolo is looking to buy Banca Monte dei Paschi di Siena in Italy for $30B, Revolut starts rolling out mobile plans in the Netherlands, Klarna launches FDIC regulated savings accounts in the US and Coinbase launches stablecoin backed credit cards. In the VC ecosystem, Creator Fund closes a new $56M fund, THENA Capital closes a $45M fund to invest in healthtech, Pitchdrive closes a $60M fund IV, Kindred Ventures a new $355M fund and Angel Invest a $40M fund to invest in early stage European founders. And finally, some very interesting funding rounds from fintech startups like Trustap, blnk, Reset, Record OS, Satispay, nesto, Digital Asset and many others.

Let’s take a closer look:

Rounds

Banco Plata secures additional $300M financing to scale in Mexico

Morpho secures $50M to scale decentralized lending infrastructure

EDGE Markets raises $29.2M Series A to build infrastructure for prediction markets

Reset raises $6M to expand embedded earned wage access for credit unions

Record OS raises $2M to modernize UK self assessment tax filing

Vinyl Equity raises $20M to modernize capital markets infrastructure for IPOs

Earlytrade raises $25M to scale construction payments infrastructure

F2 raises $24M to scale AI infrastructure for private credit

Capsa AI raises $18M to scale private capital operating system

paymove secures €2.12M to expand AI payment infrastructure in Europe

Italian fintech Satispay plans €120M capital increase to build a full financial platform

KOHO raises $130M as it moves closer to a Canadian banking license

nesto raises $302M at $1.47B valuation to scale AI mortgage technology

Digital Asset raises $355M round led by a16z crypto

Titan raises $3M to build banking native AI infrastructure

Trustap raises €8.7M to build the payment layer for AI shopping agents

VC funds

Creator Fund closes $56M fund to back Europe’s scientific founders

THENA Capital closes £45M Fund I to back UK medtech startups

Pitchdrive closes €60M fund IV to back AI native early stage startups

Kindred Ventures raises $355M to back the next wave of AI startups

Angel Invest closes €40M fund III to back Europe’s earliest startups

News on the market

Intesa Sanpaolo launches €30.6B offer for Banca Monte dei Paschi di Siena

Revolut weighs secondary share sale at $115B valuation

Bending Spoons files for Nasdaq IPO after surpassing $1B in revenue

Adyen shares drop after critical Cleveland Research Company report

Airwallex acquires Leapfin to expand finance automation capabilities

Qonto partners with Upvest to bring money market funds to European SMEs

Trade Republic fined €2.5M by Italian Antitrust authority over saveback marketing

Monzo and Fair4All Finance partner to expand credit access in the UK

BoursoBank to integrate Wero instant payments by end 2026

Coinbase and Cardless launch stablecoin secured credit card

Figure to acquire Kiavi in $717M real estate lending deal

Banca centrale europea pushed Revolut to strengthen controls during European expansion

Mastercard partners with Sapiom to launch Agent Pay for Machines

Barclays to acquire GoHenry to expand youth banking in the UK

Adyen to acquire Orb for $335M to connect billing and payments

And here some useful resources for everyone involved in the ecosystem:

Events you don’t want to miss

London tech week | London | 08-12 June (link here)

Swiss fintech week | Zurich | 19-25 June (link here)

We make future | Bologna | 24-26 June (link here)

Dutch blockchain week | Amsterdam | 22-28 June (link here)

You have a cool event you want to mention or to sponsor? Feel free to send me a DM.

Founders to watch in fintech

I also wanted to start shining a light on the most interesting fintech founders out there, so I thought to start sharing how I look for ideas to invest on. Every week, I will start sharing the most interesting founders in fintech, divided per area.

This week I am taking a look at the most interesting fintech startups in Spain! And you can already see a couple of interesting founders in stealth!

I usually use Spectre to scout for new ideas, the team is great and they also give me a free account once they learned I was a fan of the product. So if you wanna take a look at it, you can find it here.

VCs and PEs raising new funds now

I would like to leave this part of the newsletter as space for VC and solo GP that are launching new funds right now. I frequently speak with GPs and LPs, and I like the idea of giving them a showcase where to announce what they are doing. Here the new funds raising right now that I have been talking with:

Parallax Ventures, a fintech VC fund focused on Latam. They closed Fund I with a strong +50% IRR and 0.7x DPI, and are now raising Fund II. Take a look here if you want to know more or reach out directly to the GP at gennari@parallax.vc for details.

Founder Factor, VC focused on YC companies, that just closed investments on the latest YC W26. They are expanding the current vehicle to double down on the current batch. You can take a look here if you are interested.

RedFish Capital Partners, a private equity investor focused on Italian SMEs in growth and mature capital phases, with a track record exceeding 40% IRR and with over €200M in Assets. Currently raising its brand new AIF, which has already secured a soft commitment from the European Investment Fund (EIF). You can check them out at redfish.capital or contact the team at investor.relations@redfish.capital.

Overall, very interesting to see where the VC ecosystem is heading recently, between new emerging managers, solo GP and micro funds.

Always happy to support if I can! If you are raising a fund and you want to be listed here send me a message on Linkedin.

And finally, take also a look at the last edition of the newsletter, Weekly update #135