Weekly update #135

The latest news from the fintech and VC ecosystems

Welcome to this edition of the weekly newsletter. The idea behind this is to gather all the information in the startup ecosystem in one place, with a special focus on the fintech market and the VC industry.

The latest episode of Builders has been released this week! In this episode, I sit down with Sander Janca-Jensen, CEO and co-founder of Flatpay. You can watch the full episode here on YouTube, or listen to it here on Spotify or here on Apple Podcast. But take a look at a quick clip first:

Sander is the CEO and cofounder of Flatpay, the Danish fintech company building payments, point of sale and financial services for small and medium sized physical merchants, including restaurants, cafés and independent shops.

Founded in 2022, Flatpay has quickly become one of Denmark’s fastest growing fintech scaleups, reaching unicorn status after a €145 million funding round that valued the company at around €1.5 billion, up from roughly $100 million in 2024.

Before launching the company, he spent almost six years at Verisure, where he held senior roles including Deputy Managing Director and Field Sales Director, managing more than 450 salespeople and overseeing around DKK 300 million in annual profit and loss responsibility. Earlier in his career, he held multiple sales leadership roles at Berlingske Media and cofounded SimplyJob, which reached more than 125,000 users within one year before its exit in 2018.

With him, we will talk about the importance of physical sales in payments, hiring in fast growing environments, and the fintech trends in the payment space in Europe.

Coming back to us, I’ve been reading a very interesting report this week, the “Global banking annual review 2026” by McKinsey & Company. The paper is a preview of the annual report shared by the famous consulting group, with a focus on the major trends in the banking sector across countries and segments. Here my main takeaways:

In 2025, global banking continued to expand, with margins remaining high and broadly stable. However, banks are capturing a smaller share of global funds, as more financial assets move beyond traditional balance sheets, changing how the sector generates revenues and profits.

A key trend was the growing importance of regional banking models. Banks in different parts of the world increasingly operate in distinct ways, and their performance reflects those differences. This regional divergence, combined with scalable new technologies, is creating opportunities for new models of banking expansion.

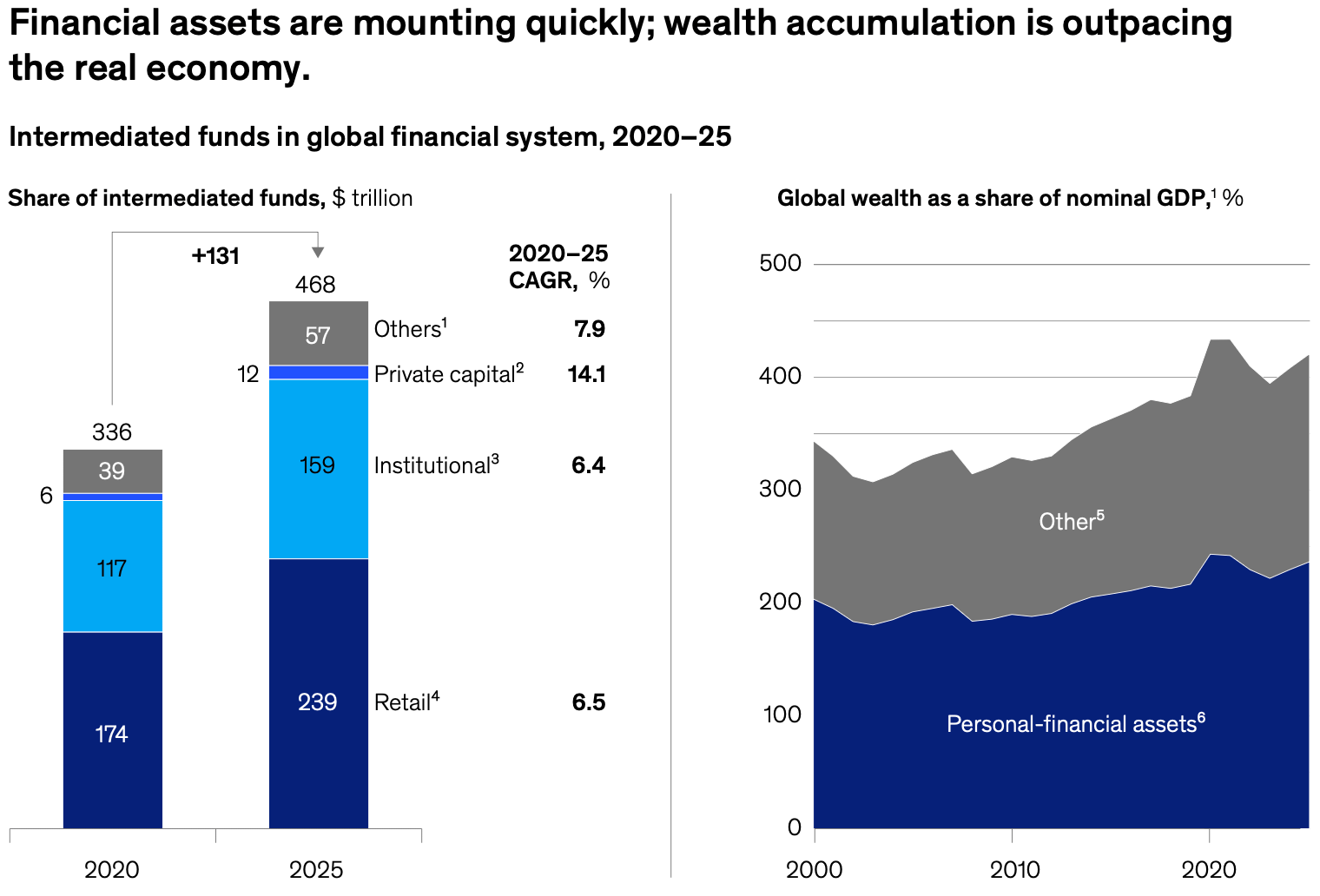

From 2020 to 2025, funds intermediated by the global financial system grew by $131 trillion, reaching $468 trillion. All categories expanded faster than nominal GDP, while private capital grew the fastest, at a 14.1% annual rate. Despite this, retail banking remains the largest global repository of accumulated wealth.

In 2025, rising capital flows supported stronger banking revenues and profits. Bank held balances, including deposits, loans, and assets under management, increased from $381 trillion in 2024 to $406 trillion in 2025. Revenues before risk costs rose from $6.1 trillion to $6.4 trillion, while profits grew 7% year on year to $1.3 trillion.

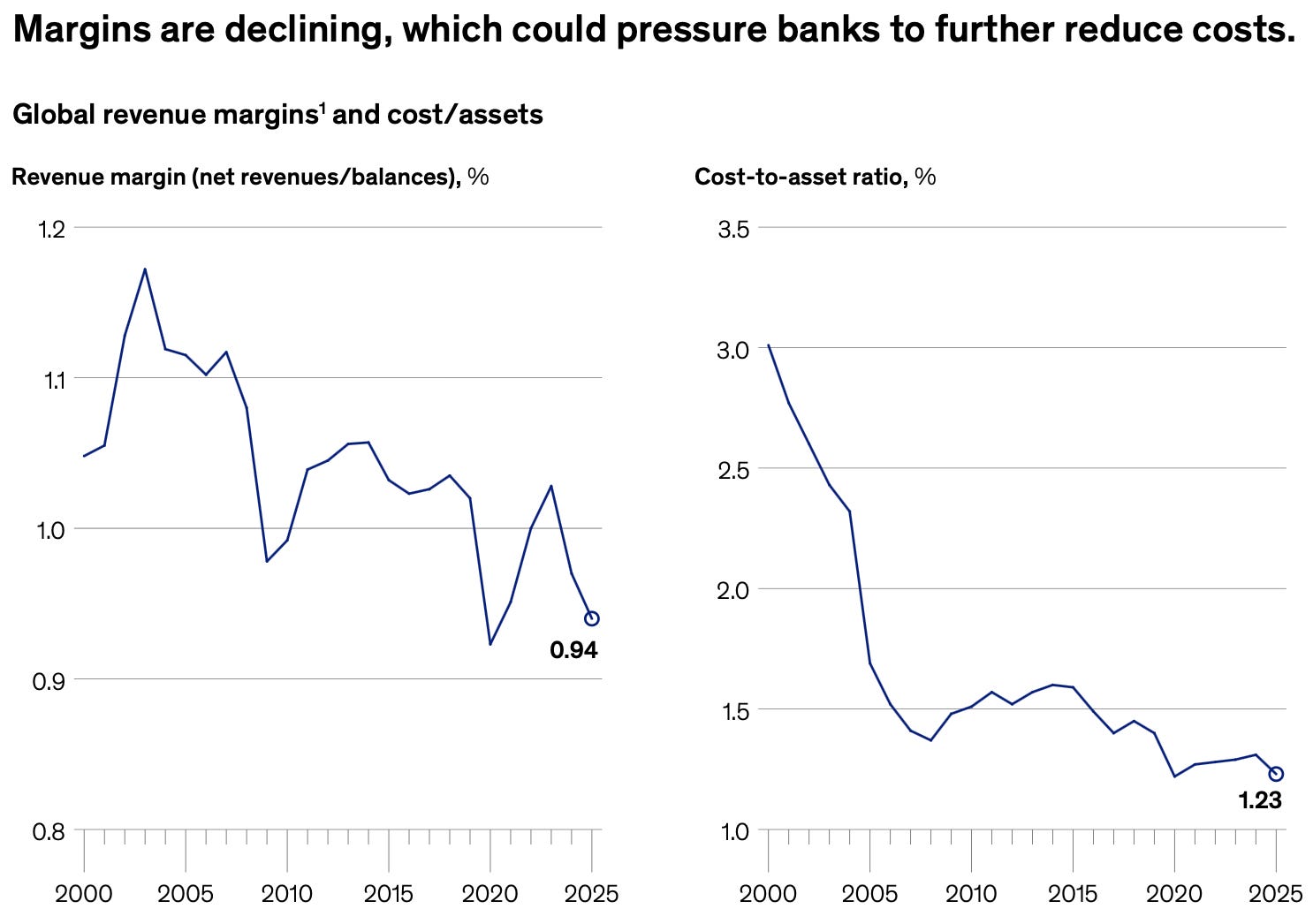

Margins stayed broadly stable, although revenue margins edged down from 0.97% in 2024 to 0.94% in 2025. Costs improved, falling from 1.31% of assets to 1.23%, but revenue margins remain below early 2000s levels.

Banks’ economics are also shifting. Of the $468 trillion in the global financial system, the on balance sheet share declined from 44% in 2022 to 40% in 2025. Transaction banking and distribution now generate 47% of revenues and 57% of profits.

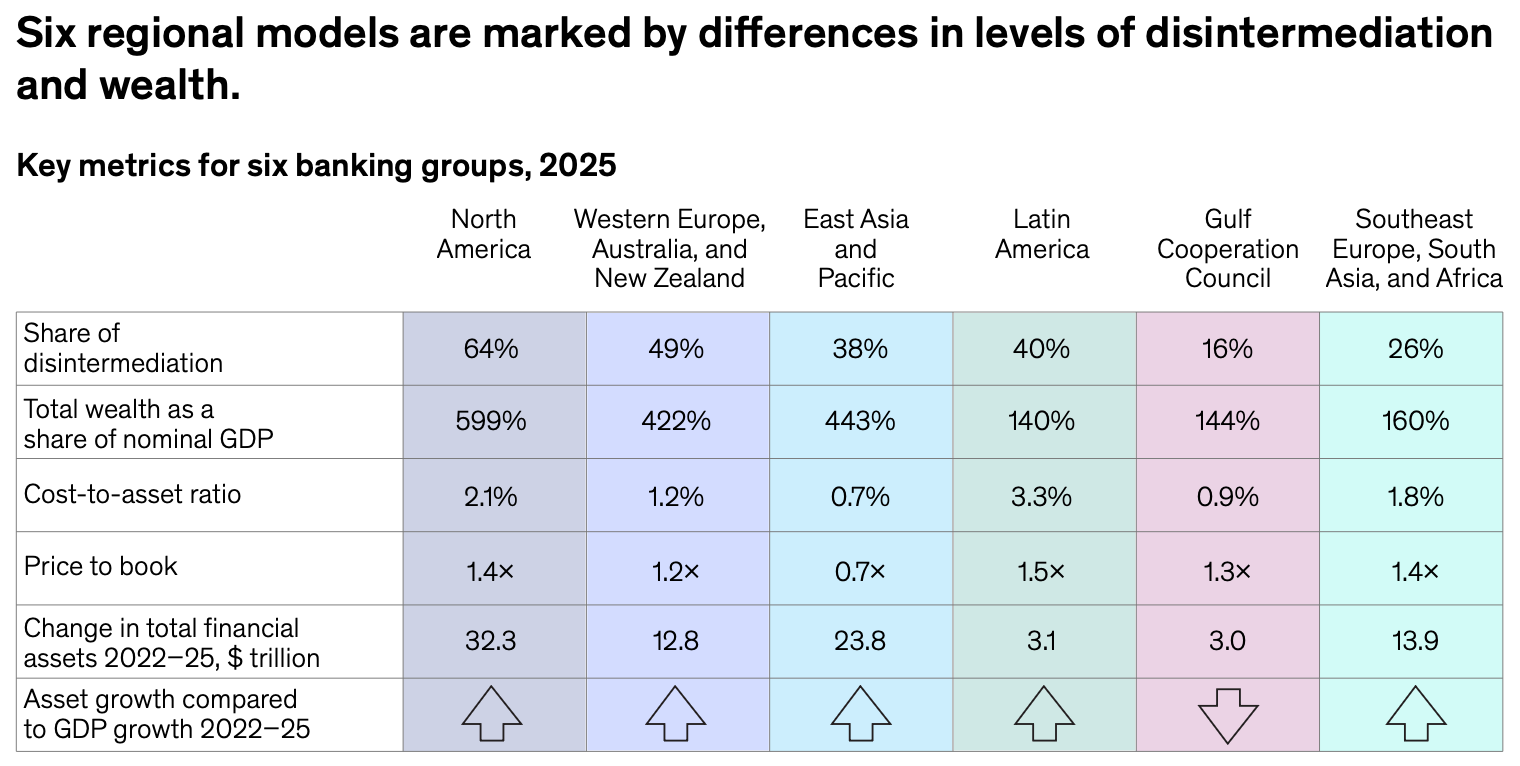

As geopolitical shifts reshape trade, manufacturing, and capital flows, banking strategies are becoming more regionally distinct. Following the movement of wealth shows North America gaining ground, supported by stronger growth in the United States and Canada. From 2022 to 2025, North American intermediated funds grew 8%, driven largely by inflows into US asset managers. European wealth expanded at roughly half that pace, while Latin America grew quickly but still below GDP growth.

Despite a lower gross savings rate than the European Union, at 18% versus 25%, the United States continues to attract a larger share of global flows due to confidence in its financial system. This helped lift US banking ROE to 12%. European banks also improved, with ROE rising from 10.7% in 2024 to 11.6% in 2025, while Western European bank shareholder returns surged 62.9 basis points.

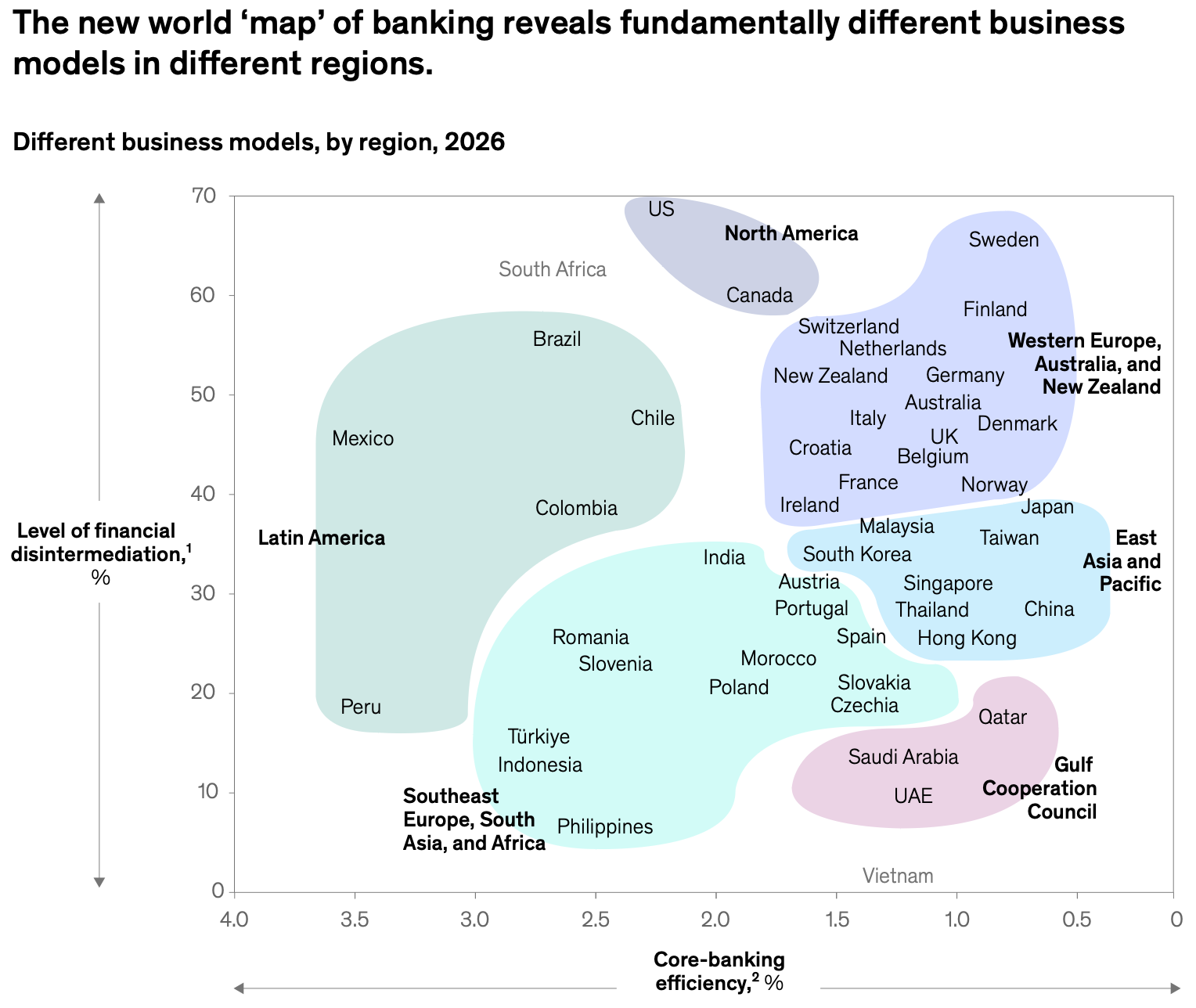

Regional banking models differ significantly in their reliance on balance sheets, capital markets, and cost efficiency. North America has historically been more disintermediated than other regions, supported by deep capital markets and banks’ greater use of corporate bonds instead of loans held on balance sheets.

Gulf Cooperation Council banks remain among the most balance sheet dependent, but offset this with strong cost efficiency. Banks in Northwest Europe, Australia, and New Zealand are close to US peers in reducing balance sheet reliance and are generally more efficient. Sweden and Finland stand out as strong examples, combining low balance sheet dependence with high efficiency, suggesting a possible model for a more resilient and lower transaction cost financial system.

Elsewhere in Europe, banks remain more dependent on balance sheets, while operating costs are generally higher.

Money20/20 was a blast! Great energy, lots of interesting companies, amazing event!

I also recorded a special episode of #Builders live with Martina Weimert , CEO of EPI Company, the corporation behind popular payment method Wero. Can’t wait to release it!

But let’s take a closer look at the main news of the last seven days. Deel released stablecoin wallet for global contractors, ING expanded Wero for online payments to 10M customers in Germany, Checkout.com partners with Coinbase to bring stablecoin payments to merchants, OpenFX agreed to acquire Embed. But also, Revolut CEO Nik Storonsky named and banker of the year 2025 and CTO Vlad Yatsenko moving to a board role, Klarna released an in app inbox to protect users from scams, Adyen selected to power payments for GOV.UK and Triple-A secured a MiCA license. In the VC ecosystem, Gigascale Capital closed a $250M fund to invest in climate tech, Merantix Capital a $103M fund to back European founders and Benchmark a $2B first growth fund. And finally, some very interesting funding rounds from fintech startups like Fonoa, Gradient Labs, Aveni, Ramp, Kodesage, Paypercut and many more.

Let’s take a closer look:

Rounds

Fonoa raises €94.4M Series C and acquires Tax Edge from PwC

Saris AI raises $28.8M series A to scale agentic workflows for banks and credit unions

Gradient Labs increased its Series A to $26M to build AI agents for financial services

Bayshore AI raises $8M to bring AI powered automation to compliance

Paypercut raises €5M to scale payments infrastructure across CEE

Aveni raises £12M to expand AI governance for financial services

Ramp raises $750M at $44B valuation to expand AI powered finance platform

Kodesage raises $6.6M to modernise legacy financial software with on premise AI

WasabiCard raises nearly $10M to scale stablecoin payment infrastructure

Cense raises €6.5M seed round to expand crypto compliance platform

VC funds

Former Meta CTO closes $250M fund to back deeptech climate founders

Merantix Capital closes €103M fund to back European AI startups

News on the market

Triple-A secures MiCA CASP license for EU stablecoin payment services

OpenFX agrees to acquire Embed to strengthen European payments infrastructure

Mastercard joins European pilot for instant cross border payments

Silverflow targets international growth as transactions approach 1B annually

Coinbase opens regulated access to global crypto derivatives for US institutions

FalconX files confidentially for IPO after 21shares acquisition

Revolut CEO Nik Storonsky named European banker of the year 2025

BUUT Pay brings mobile payments to Dutch teens under 16

Checkout.com and Coinbase bring stablecoin payments to enterprise merchants

Robinhood enters Canada after completing WonderFi acquisition

Revolut begins controlled India rollout ahead of wider launch

OKX Ventures takes 19.6% stake in South Korea’s 코인원 Coinone

Ripple expands RLUSD stablecoin to Türkiye through new institutional partnerships

MoneyGram launches MGUSD stablecoin on Stellar Development Foundation

Apple expands payments ambitions with AI powered bill splitting feature

ING expands Wero to online payments for 10M customers in Germany

TrueLayer launches Bank on File for recurring pay by bank payments

TransferMate Global Payments partners with BVNK to add stablecoin rails to global B2B payments

Adyen selected to power GOV.UK Pay’s next phase of public sector payments

Affirm and Stripe Expand partnership to bring pay over time to UK merchants

Revolut US bank plans stablecoin services alongside FDIC insured products

Klar acquires Yave to enter Mexico’s digital mortgage market

Keyrock to acquire bankrupt crypto firm BlockFills for $3.25M

Revolut cofounder Vlad Yatsenko moves from CTO to board role

Klarna introduces in app inbox to help users identify scams

Consortium backed by J.P. Morgan and Citi plan tokenized deposit network for 2027

And here some useful resources for everyone involved in the ecosystem:

Events you don’t want to miss

SuperReturns | Berlin - 08-10 June (Link here)

You have a cool event you want to mention or to sponsor? Feel free to send me a DM.

Founders to watch in fintech

I also wanted to start shining a light on the most interesting fintech founders out there, so I thought to start sharing how I look for ideas to invest on. Every week, I will start sharing the most interesting founders in fintech, divided per area.

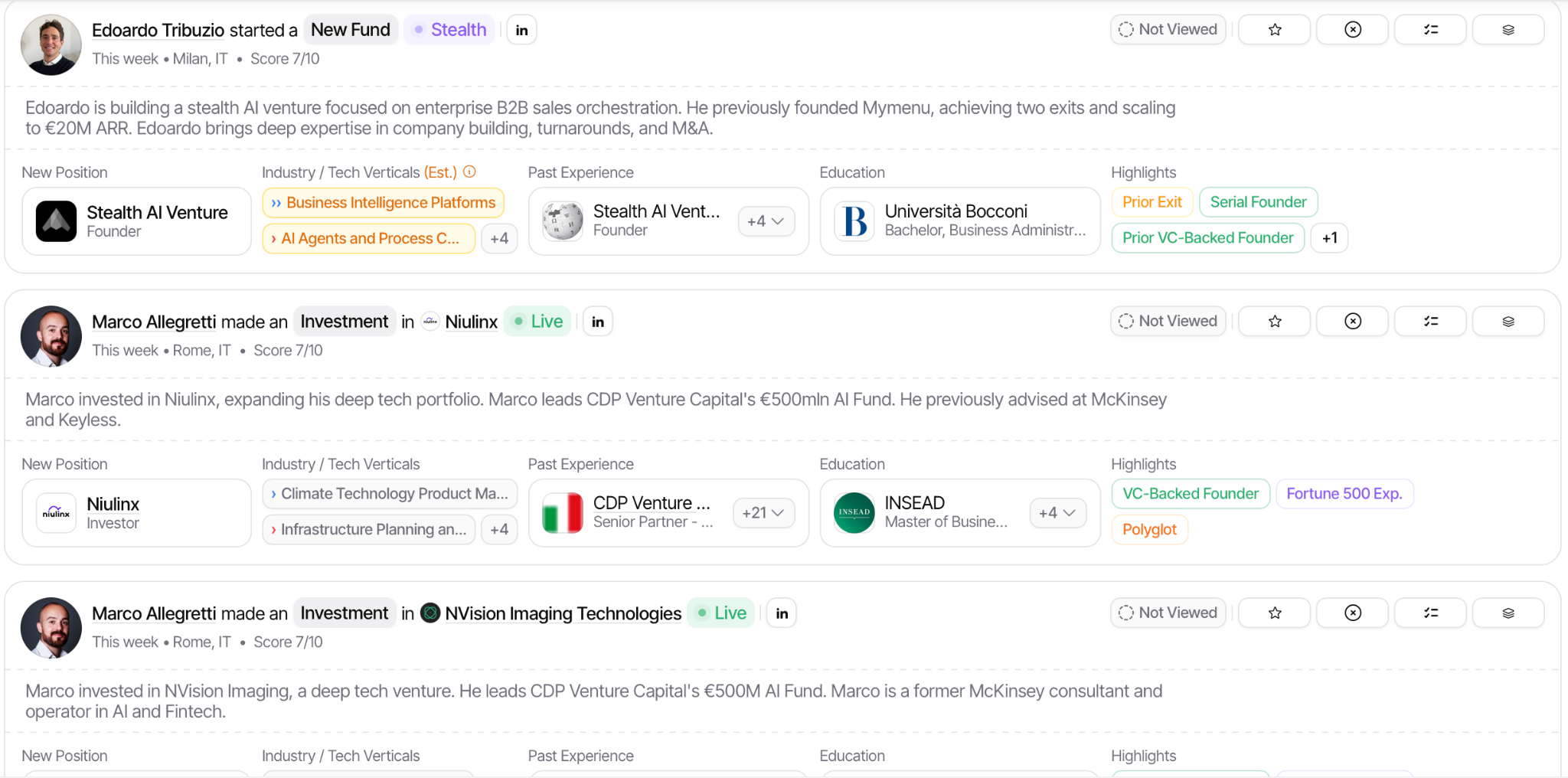

This week I am taking a look at the most interesting founders in fintech in my own country, Italy. And you can already see a couple of interesting founders in stealth!

I usually use Spectre to scout for new ideas, the team is great and they also give me a free account once they learned I was a fan of the product. So if you wanna take a look at it, you can find it here.

VCs and PEs raising new funds now

I would like to leave this part of the newsletter as space for VC and solo GP that are launching new funds right now. I frequently speak with GPs and LPs, and I like the idea of giving them a showcase where to announce what they are doing. Here the new funds raising right now that I have been talking with:

Parallax Ventures, a fintech VC fund focused on Latam. They closed Fund I with a strong +50% IRR and 0.7x DPI, and are now raising Fund II. Take a look here if you want to know more or reach out directly to the GP at gennari@parallax.vc for details.

Founder Factor, VC focused on YC companies, that just closed investments on the latest YC W26. They are expanding the current vehicle to double down on the current batch. You can take a look here if you are interested.

RedFish Capital Partners, a private equity investor focused on Italian SMEs in growth and mature capital phases, with a track record exceeding 40% IRR and with over €200M in Assets. Currently raising its brand new AIF, which has already secured a soft commitment from the European Investment Fund (EIF). You can check them out at redfish.capital or contact the team at investor.relations@redfish.capital.

Overall, very interesting to see where the VC ecosystem is heading recently, between new emerging managers, solo GP and micro funds.

Always happy to support if I can! If you are raising a fund and you want to be listed here send me a message on Linkedin.

And finally, take also a look at the last edition of the newsletter, Weekly update #134