Weekly update #133

The latest news from the fintech and VC ecosystems

Welcome to this edition of the weekly newsletter. The idea behind this is to gather all the information in the startup ecosystem in one place, with a special focus on the fintech market and the VC industry.

The latest episode of Builders has been released this week! In this episode, I sit down with Bhavin Shah, founder and CEO of Sherlocq. You can watch the full episode here on YouTube, or listen to it here on Spotify or here on Apple Podcast. Here a shot clip from the video:

Bhavin is the Founder and CEO of Sherlocq, an AI-powered regulatory intelligence company helping compliance professionals, law firms, and regulators navigate complex global regulations with greater speed, accuracy, and security. With more than 20 years of experience across the U.S., UK, Middle East, and Asia, Bhavin has built a global reputation in financial crime, compliance, investigations, and governance.

Before launching Sherlocq, he held senior leadership roles at Deloitte, PwC, EY, Roland Berger, Forensic Risk Alliance, and Secretariat, advising global banks, sovereign institutions, private equity firms, and digital platforms on high-stakes regulatory matters. Bhavin is also a World Economic Forum Young Global Leader, a recognised thought leader in AI and compliance, and an advisor on financial and regulatory innovation.

With him, we will talk about the fintech market in the MENA region, how regulations are shaping this market, but also the differences between investing in fintech in different parts of the world.

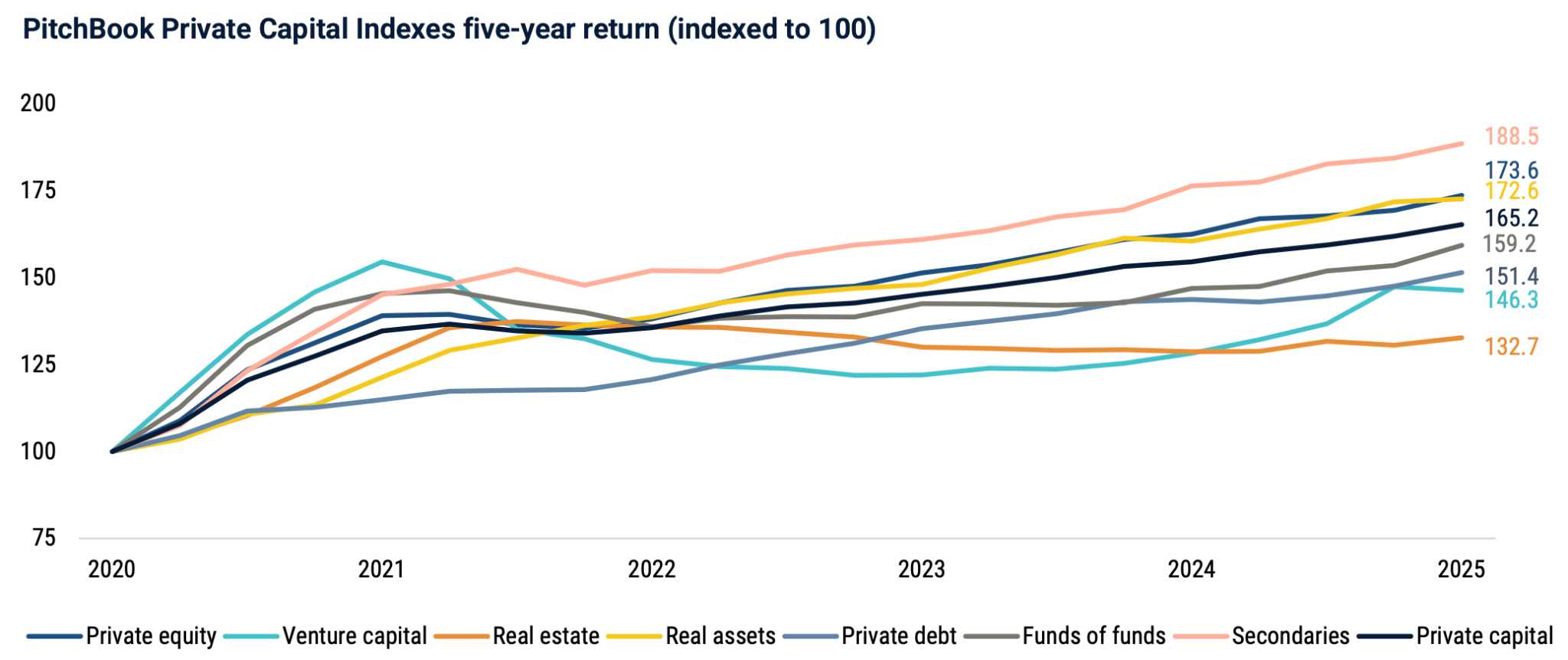

Coming back to us, I’ve been reading a very interesting report this week, the “Private capital index returns Q4 2025” from PitchBook. The PitchBook Private Capital Indexes are quarterly return benchmarks for the private market industry. These indexes are built with fund cash flow and NAV data, to give clear indications on funds’s returns over a specific period of time. Here my main takeaways:

Private capital delivered solid returns over the past five years, with all major PitchBook indexes above their 2020 starting point. Secondaries led the market, reaching 188.5 on an indexed basis by 2025, followed by private equity at 173.6 and real assets at 172.6. The broader private capital index also performed strongly at 165.2, while funds of funds and private debt reached 159.2 and 151.4 respectively. Venture capital showed a different trajectory: after a sharp rise in 2021, it declined through 2022 and 2023 before partially recovering to 146.3. Real estate was the weakest performer at 132.7, reflecting a more challenging environment for the asset class.

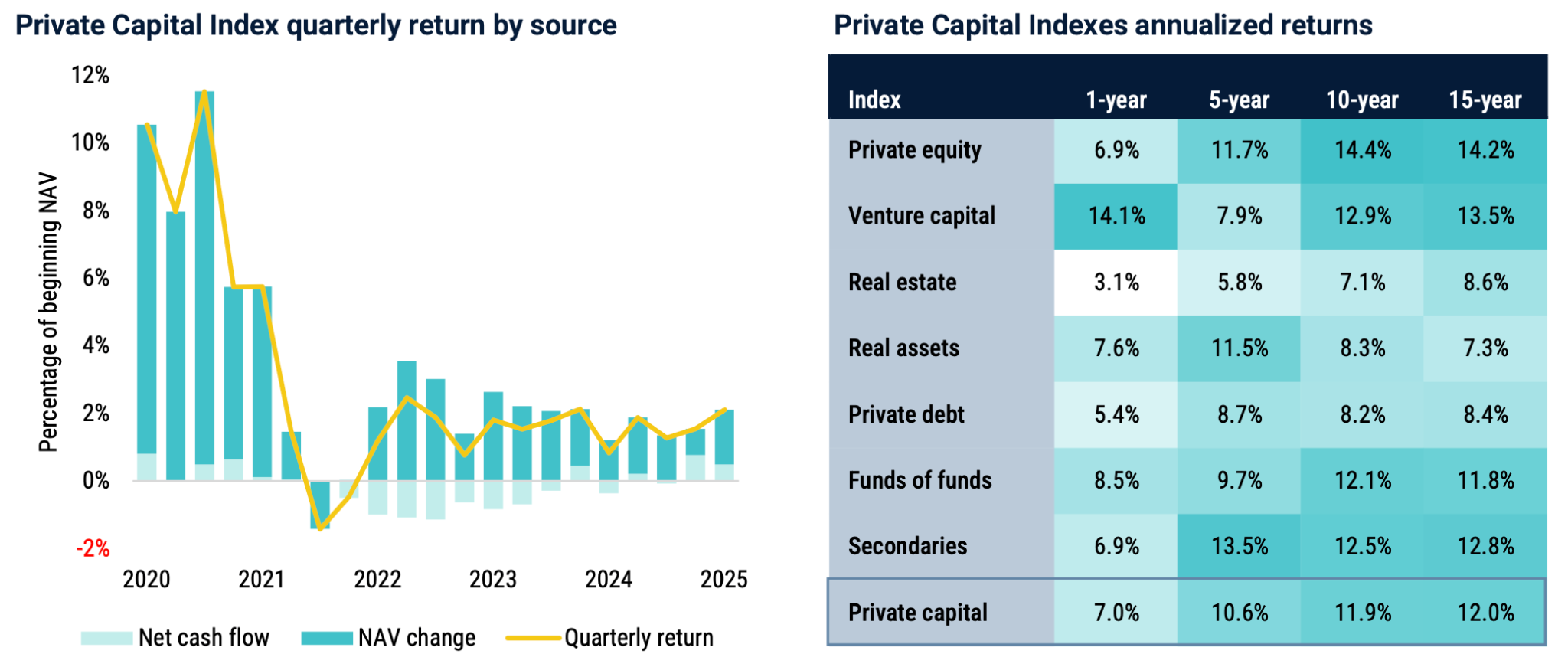

Private capital returns remained positive in early 2025, although quarterly performance has normalized after the sharp rebound seen in 2020 and 2021. The Private Capital Index quarterly return stood at around 2%, supported mainly by NAV growth, while net cash flow remained close to neutral. This suggests a steadier environment, with value creation contributing more than capital movements.

Annualized returns show private capital at 7.0% over one year, 10.6% over five years, 11.9% over ten years, and 12.0% over fifteen years. Secondaries posted the strongest five year return at 13.5%, while private equity led over ten and fifteen years with 14.4% and 14.2%. Venture capital remains competitive over longer periods, but its five year return of 7.9% reflects the recent reset in growth valuations.

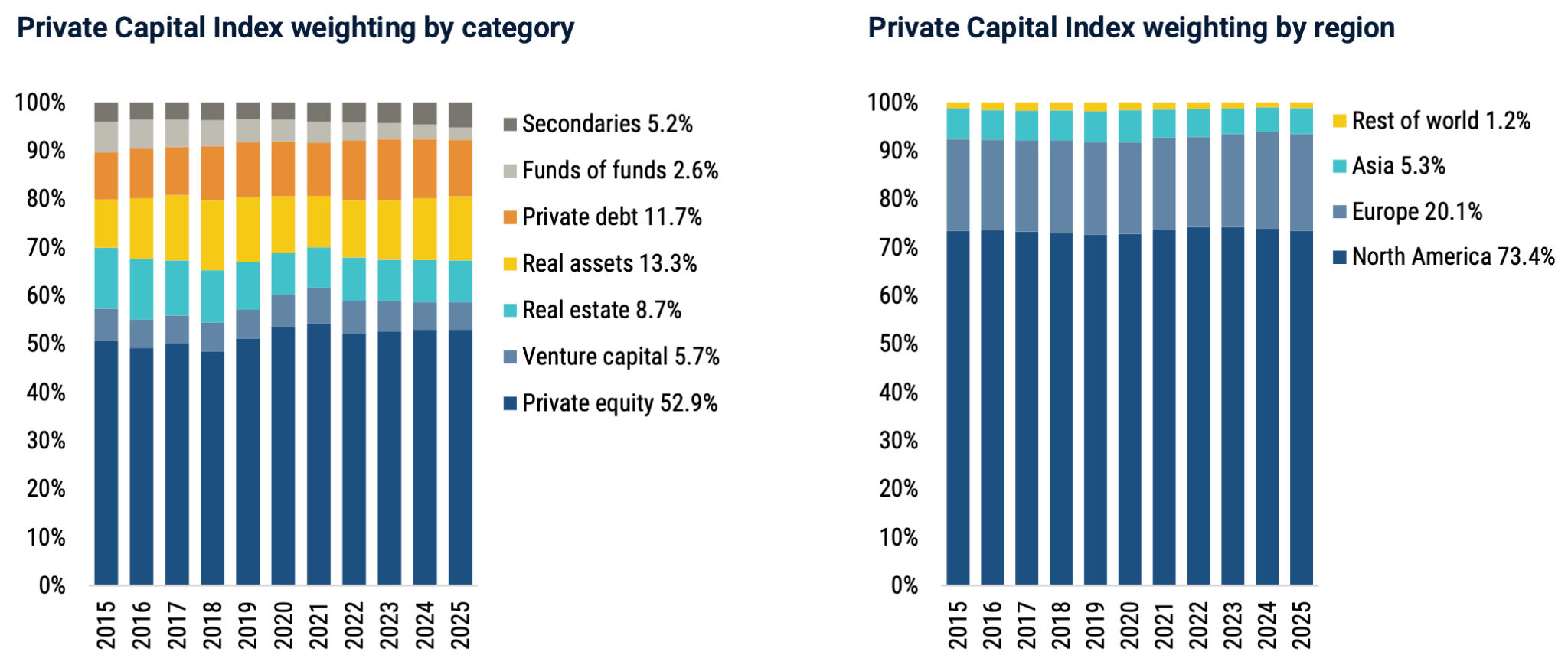

The Private Capital Index remains heavily concentrated in private equity, which accounted for 52.9% of the index in 2025, confirming its role as the main driver of overall performance. Real assets followed at 13.3%, while private debt represented 11.7%, reflecting the growing importance of income oriented strategies in a higher rate environment. Real estate stood at 8.7%, venture capital at 5.7%, secondaries at 5.2%, and funds of funds at 2.6%. From a regional perspective, the index is still dominated by North America, which represented 73.4% in 2025, far ahead of Europe at 20.1%, Asia at 5.3%, and the rest of the world at 1.2%.

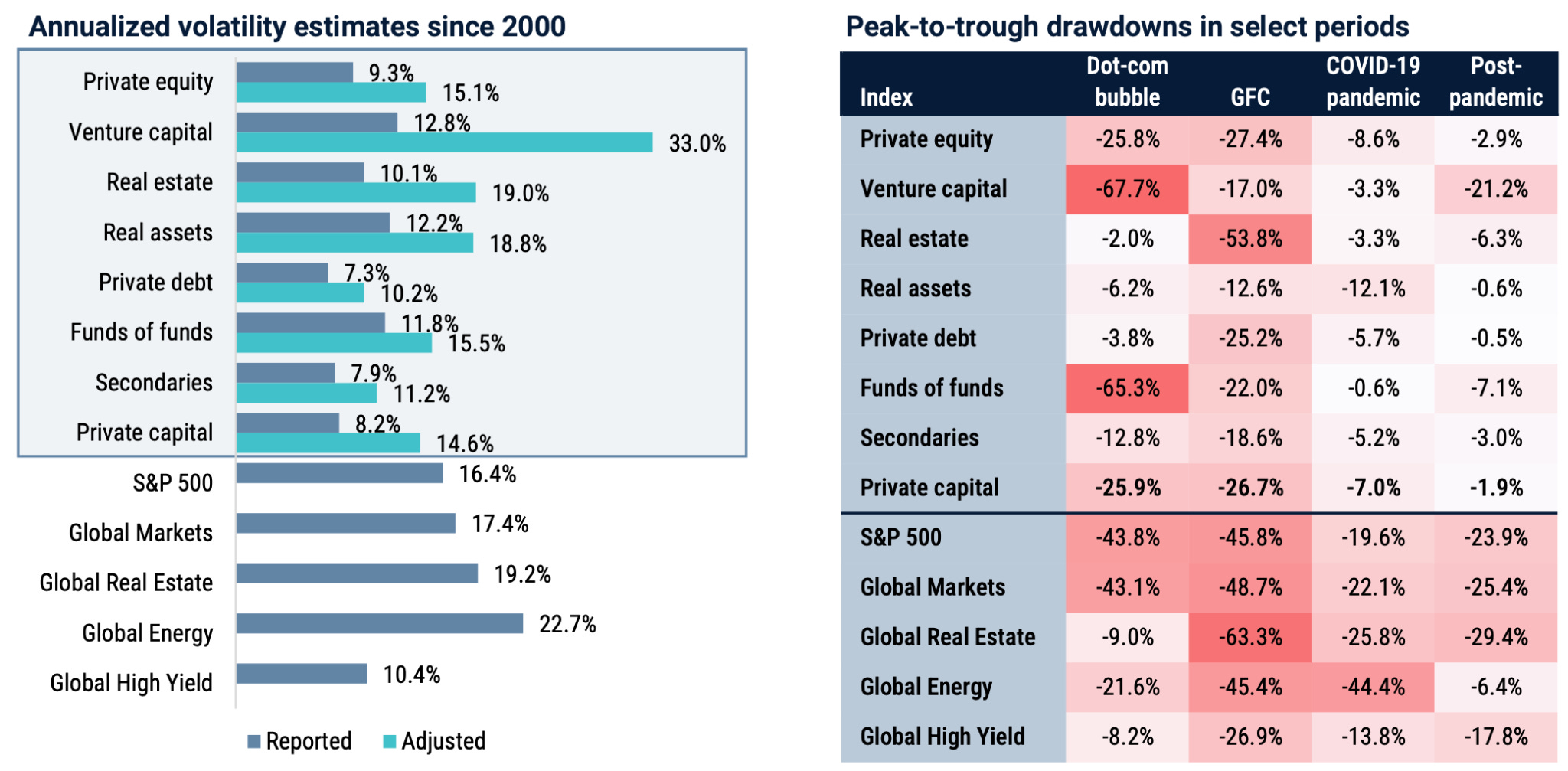

Private capital has shown lower reported volatility than public markets, with the broad Private Capital Index at 8.2% since 2000 compared with 16.4% for the S&P 500 and 17.4% for global markets. However, adjusted volatility is higher at 14.6%, suggesting that private fund valuations may smooth part of the underlying risk. Venture capital stands out as the most volatile private strategy, with adjusted volatility of 33.0%, while private debt remains the most stable at 10.2%. Drawdowns also vary sharply by period. Private capital fell 25.9% during the dotcom bubble and 26.7% during the global financial crisis, but only 7.0% during COVID and 1.9% post pandemic.

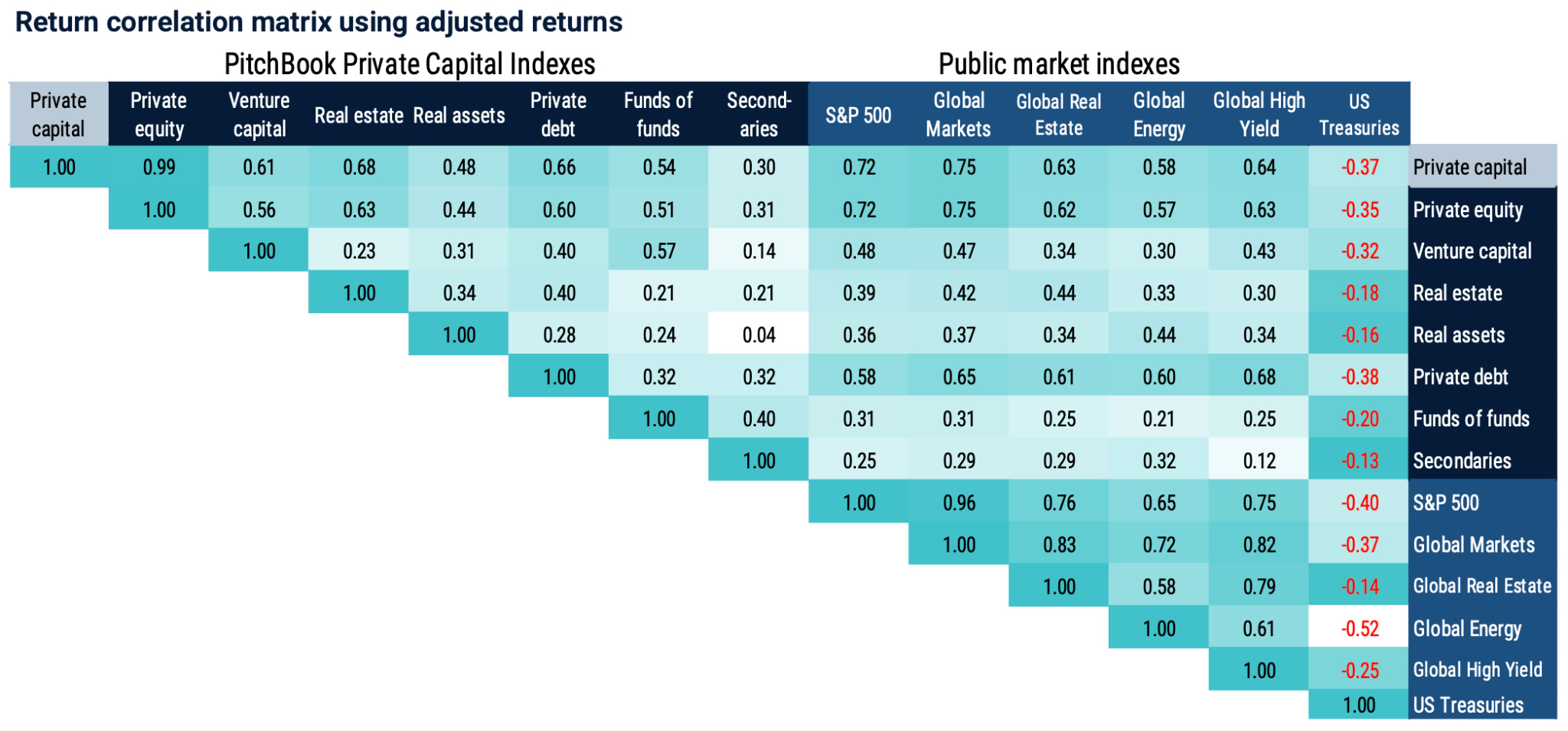

The adjusted return correlation matrix shows that private capital remains closely linked to broader risk assets, but still offers diversification benefits in specific areas. The broad Private Capital Index has a strong correlation with private equity at 0.99 and meaningful correlations with public markets, including 0.72 with the S&P 500 and 0.75 with global markets. Private debt is also relatively connected to public credit and equities, with a 0.68 correlation to global high yield and 0.58 to the S&P 500.

By contrast, secondaries show lower correlations across most categories, including 0.25 with the S&P 500 and 0.30 with private capital, suggesting a more differentiated return profile. US Treasuries remain negatively correlated across all major private capital segments, reinforcing their role as a portfolio stabilizer during risk market stress.

Also, in 2 weeks it is going to be Money20/20 time again! I will be attending and speaking in a couple of panels, happy to catch up if you are attending too!

But let’s take a closer look at the main news of the last seven days. Revolut launched the first physical crypto card that illuminates when tapping, Deel launched stablecoin payouts for payrolls, J.P. Morgan launched Chase in Germany and zerohash secured an EMI license from Dutch national bank. But also, Tether.io invested in LemFi, Bending Spoons completed Tractive acquisition, Anthropic acquired Stainless and Worldline partners with Klarna on BNPL solutions. In the VC ecosystem, Mouro Capital closes $400M for new fintech fund, EQT Group selected to lead new EU $5B deeptech fund, British Business Bank invests $25M in new Antler’s fund. But also new funds from Meridian Ventures, Eighteen48 Partners, Skybound Venture Capital, Cleo Ventures. And finally, some very interesting funding rounds from fintech startups like Primer, Moment, Mercury, Relay, Farther, Lexroom and many others.

Let’s take a closer look:

Rounds

LawX raises €7.5M to build AI operating system for Europe’s legal industry

Cosmico Italia raises €12M and acquires Flatmates to scale its future of work platform

Allica Bank secures £350M British Business Bank backing to expand SME lending

Lexroom raises $50M Series B to scale legal AI infrastructure across Europe

bunch raises $35M Series B to modernise private markets operations with AI

getquin raises €12M to build Europe’s next generation wealth platform

Moment raises $78M as AI reshapes wealth management infrastructure

Primer raises $100M Series C to build AI infrastructure for global payments

Aryze raises €3M to expand stablecoin and tokenised asset infrastructure

AEON Protocol secures $8M to build AI native settlement infrastructure

Cauridor expands African payments infrastructure with $2M Series A

RemotePass raises $17.4M Series B to expand global payroll and hiring platform

Circle co-founder Sean Neville raises $30M for AI banking startup Catena Labs

Relay secures $50M growth investment from General Catalyst

Saudi fintech Arib raises $23.5M to expand digital financing marketplace

Scapia raises $63M from General Catalyst to expand India’s travel payments platform

Banque Nationale du Canada expands partnership with Sardine and leads $25M funding extension

Farther reaches unicorn status with $150M series D led by General Atlantic

Eisen raises $18.5M to modernize compliance infrastructure for fintech and crypto

Cycles raises $6.4M to build clearing infrastructure for crypto and stablecoin payments

VC funds

Meridian Ventures launches $35M fund to back MBA deferred founders

Eighteen48 Partners reaches €175M first close for European mid market buyout fund

Lightrock closes $500M energy access fund to scale clean energy across emerging markets

EQT Group selected to lead €5B scaleup Europe fund for deeptech investments

Mouro Capital surpasses $1B in commitments with new $400M fintech fund

Cleo Ventures launches €30M AI fund to back Europe’s next gen founders

LAUXERA CAPITAL PARTNERS closes €520M healthtech fund above hard cap in less than 18 months

Skybound Venture Capital launches $38M deeptech fund backed by European Investment Fund (EIF)

British Business Bank backs Antler’s new UK fund II with £25M commitment

News on the market

zerohash secures EMI license from Dutch Central Bank to expand stablecoin infrastructure across Europe

Tether.io invests in LemFi to expand stablecoin powered remittances across emerging markets

Bending Spoons completes acquisition of pet tech leader Tractive

Anthropic acquires Stainless to expand AI agent connectivity infrastructure

N26 launches flexible cash Fund to expand retail investment offering

NMI acquires Dwolla to expand embedded payments and A2A infrastructure

Revolut launches first physical crypto card that illuminates when you tap

Deel launches stablecoin salary payouts and creates dedicated crypto division

Worldline and Klarna expand BNPL and flexible payments across Europe

Tether.io acquires Softbank’s stake in bitcoin treasury firm Twenty One Capital

J.P. Morgan launches Chase digital bank in Germany with 4% savings offer

And here some useful resources for everyone involved in the ecosystem:

Events you don’t want to miss

You have a cool event you want to mention or to sponsor? Feel free to send me a DM.

Founders to watch in fintech

I also wanted to start shining a light on the most interesting fintech founders out there, so I thought to start sharing how I look for ideas to invest on. Every week, I will start sharing the most interesting founders in fintech, divided per area.

This week I was taking a look at what funds are mostly interested in when coming to fintech in Europe. And you can see a couple of interesting signals over there.

I usually use Spectre to scout for new ideas, the team is great and they also give me a free account once they learned I was a fan of the product. So if you wanna take a look at it, you can find it here.

VCs and PEs raising new funds now

I would like to leave this part of the newsletter as space for VC and solo GP that are launching new funds right now. I frequently speak with GPs and LPs, and I like the idea of giving them a showcase where to announce what they are doing. Here the new funds raising right now that I have been talking with:

Parallax Ventures, a fintech VC fund focused on Latam. They closed Fund I with a strong +50% IRR and 0.7x DPI, and are now raising Fund II. Take a look here if you want to know more or reach out directly to the GP at gennari@parallax.vc for details.

Founder Factor, VC focused on YC companies, that just closed investments on the latest YC W26. They are expanding the current vehicle to double down on the current batch. You can take a look here if you are interested.

RedFish Capital Partners, a private equity investor focused on Italian SMEs in growth and mature capital phases, with a track record exceeding 40% IRR and with over €200M in Assets. Currently raising its brand new AIF, which has already secured a soft commitment from the European Investment Fund (EIF). You can check them out at redfish.capital or contact the team at investor.relations@redfish.capital.

Overall, very interesting to see where the VC ecosystem is heading recently, between new emerging managers, solo GP and micro funds.

Always happy to support if I can! If you are raising a fund and you want to be listed here send me a message on Linkedin.

And finally, take also a look at the last edition of the newsletter, Weekly update #132