Weekly update #129

The lates news from the fintech and VC ecosystems

Welcome to this edition of the weekly newsletter. The idea behind this is to gather all the information in the startup ecosystem in one place, with a special focus on the fintech market and the VC industry.

The latest episode of Builders has been released this week! In this episode, I sit down with Dr. Camillo Werdich , CEO and Founder of Sinpex. You can watch the full episode here on YouTube, or listen to it here on Spotify, here on Amazon Podcast or here on Apple Podcast.

Camillo is the CEO and Founder of Sinpex, an AI-driven compliance platform focused on transforming how financial institutions manage KYC, onboarding, and regulatory workflows. Since founding the company in 2019, he has led the development of solutions leveraging large language models to improve data accuracy, automate document analysis, and adapt quickly to evolving regulatory requirements.

He brings a strong blend of technical and financial expertise, with early experience in engineering roles at ZF Friedrichshafen and Transsolar, followed by consulting at Deloitte, where he gained exposure to complex business and regulatory environments.

Dr. Werdich holds a PhD in Economics from the Universität St. Gallen-Hochschule für Wirtschafts-, Rechts- und Sozialwissenschaften, complemented by academic experience at the The London School of Economics and Political Science (LSE) and a cum laude MSc in International Business. His work sits at the intersection of AI, compliance, and financial services innovation.

With him, we will talk about how necessary and complex is KYC in fintech today, the struggle with data sources for KYB, and why regulations is critical for innovation.

Coming back to us, this week I’ve been reading a very interesting report, the “Infrastructure: investing to support global growth” from McKinsey & Company. The world has an immense need for infrastructure, a global mandate that is being met in large part with a massive influx of private capital. Over the past few years, private capital has been flowing into infrastructure assets at an unprecedented rate, mostly when coming to datacenters. Here my main take aways from the report:

Global infrastructure demand is projected to reach $106 trillion by 2040, driven by population growth and accelerating technological progress. The definition of infrastructure is also expanding beyond traditional assets such as transport and utilities to include digital and renewable sectors.

Energy and power alone are expected to require $23 trillion, supported by the energy transition and rising consumption. In the United States, power demand is forecast to grow above 3 percent annually after years of minimal expansion, despite constraints such as supply chain issues, permitting delays, and labor shortages. At the same time, digital infrastructure is scaling rapidly, with data center investments estimated at nearly $7 trillion by 2030.

Energy and digital sectors together represent about 40 percent of total infrastructure needs. Private capital plays a dominant role, accounting for roughly 75 percent of investments, as public funding faces slower processes and budget limitations.

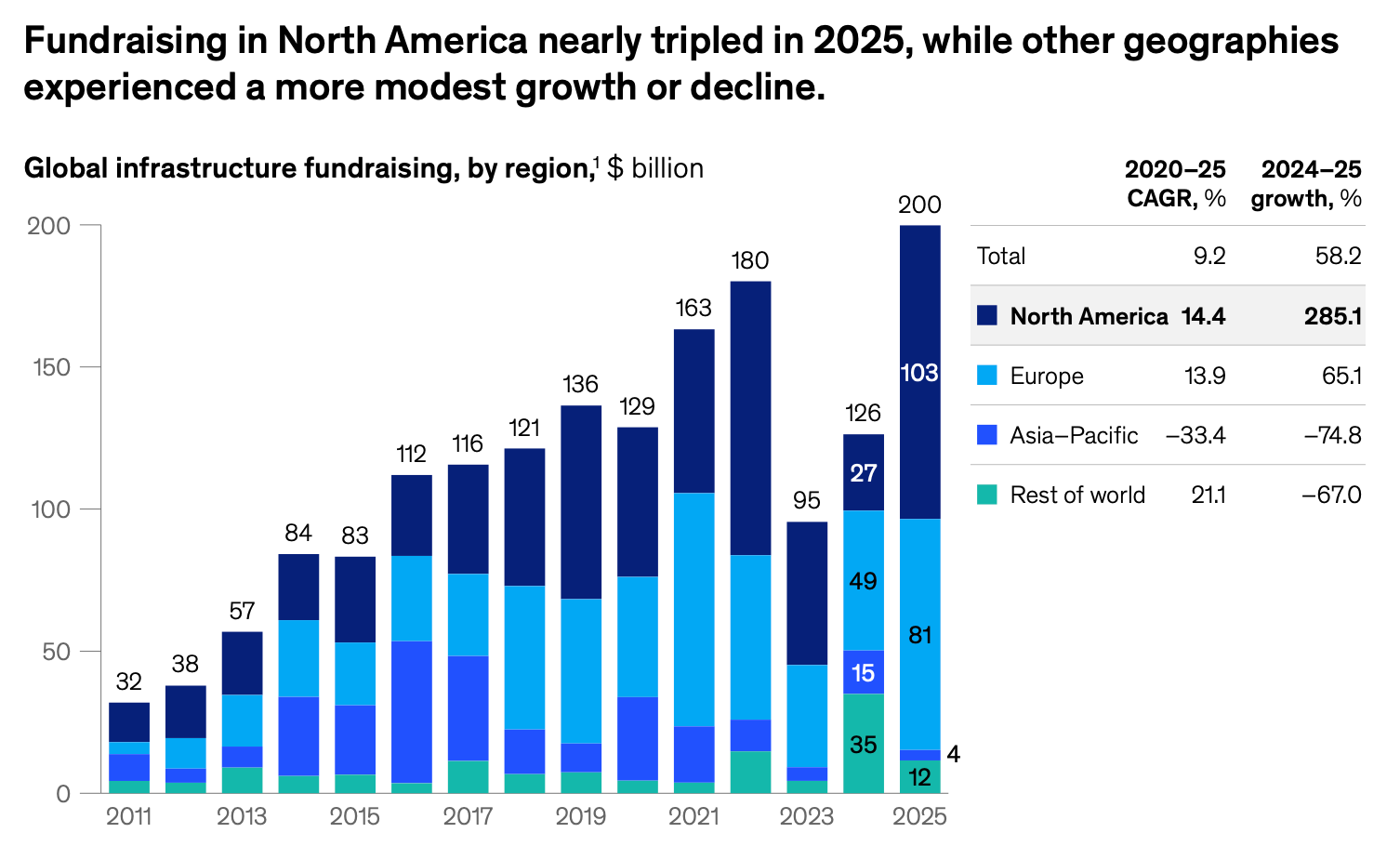

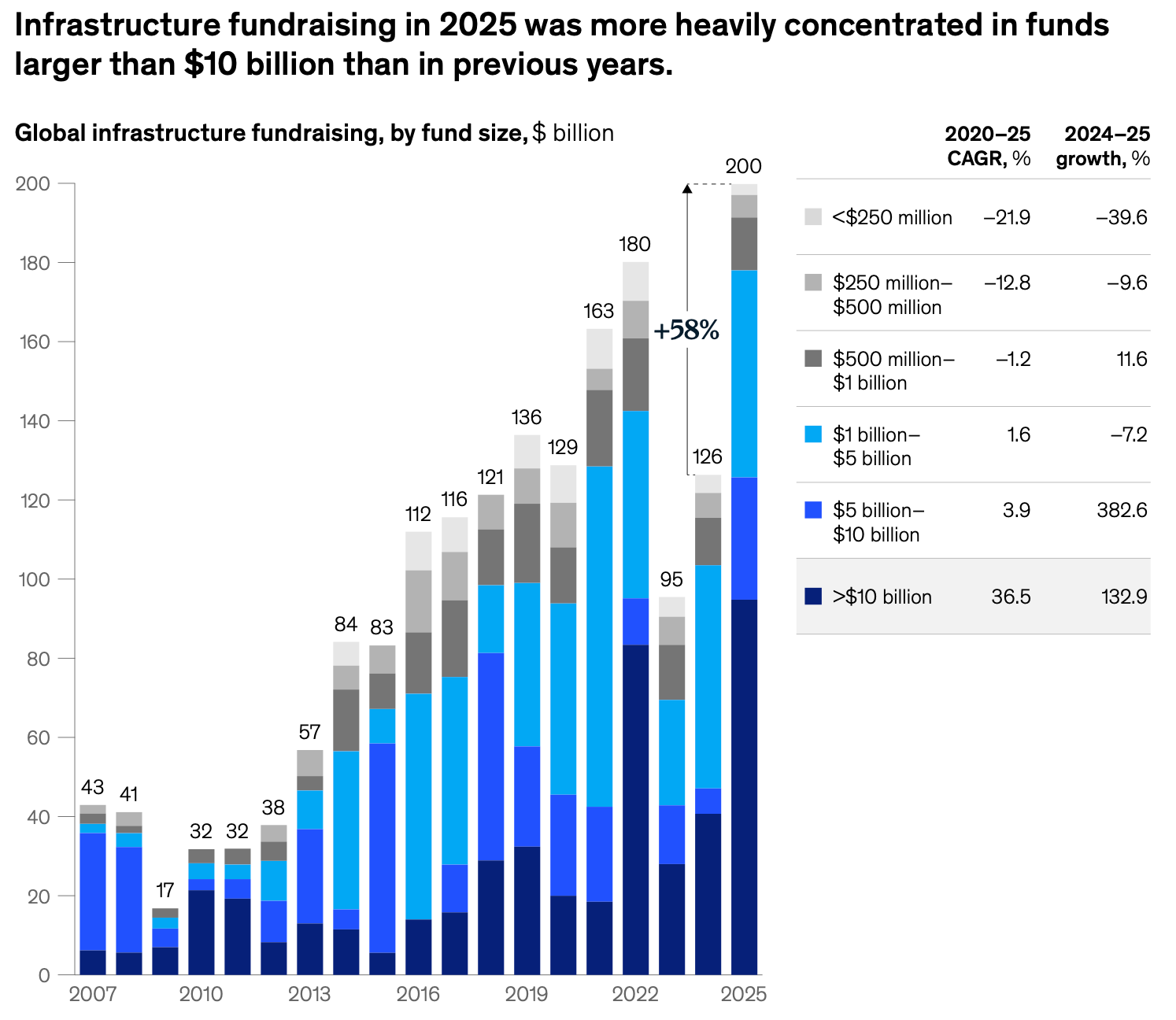

Infrastructure investment needs are vast, yet private capital continues to scale to meet demand and support long term economic growth. In 2025, infrastructure fundraising reached a record nearly $200 billion, up about 60 percent from 2024 and exceeding the previous $180 billion peak in 2022. This followed a temporary slowdown in 2023 due to rising interest rates and a shift toward debt strategies, before rebounding strongly.

Private investment also accelerated, rising from $95 billion in 2023 to $126 billion in 2024, and then surging to 2025’s record levels. Regional dynamics show mixed trends: fundraising declined in Asia Pacific but grew significantly in Europe, increasing by around 65 percent, and surged in North America by approximately 285 percent. This growth was largely driven by megafunds with more than $5 billion in committed capital, enabling large scale deployments.

Institutional investors are increasingly prioritizing infrastructure within their portfolios. A recent survey of around 300 global LPs shows that 51 percent plan to increase allocations to the asset class over the next three years, well ahead of buyout at 35 percent and real estate at 30 percent. Sovereign wealth funds, insurers, and family offices are leading this shift, with intentions rising by about ten percentage points compared to 2024.

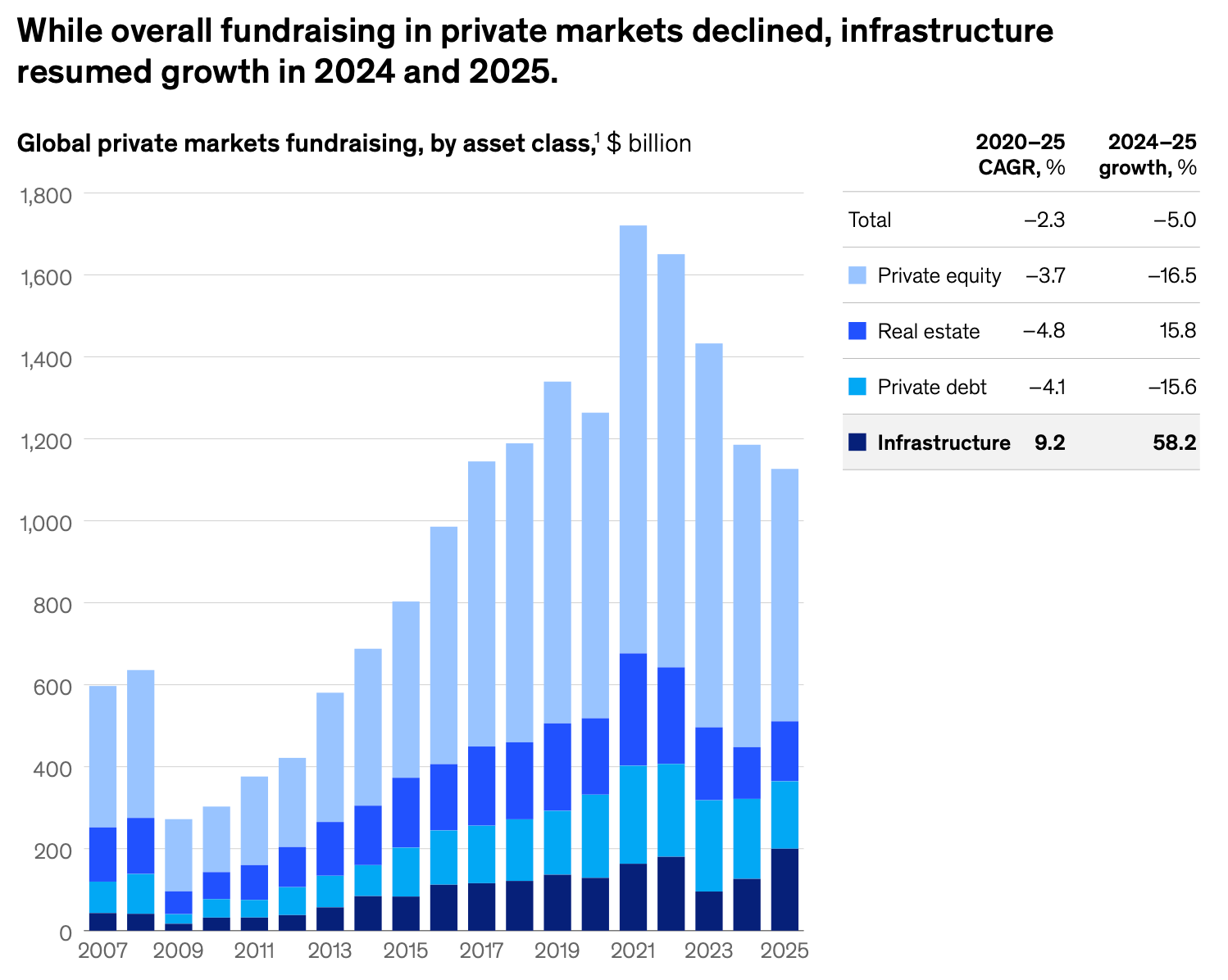

This growing demand is reflected in fundraising performance. Infrastructure has recorded a 9 percent CAGR between 2020 and 2025, while other private market asset classes have declined by roughly 3 to 5 percent. Momentum strengthened further in 2025, with fundraising increasing by more than 58 percent year over year. In contrast, real estate grew by about 16 percent, and several other asset classes experienced contractions, reinforcing infrastructure’s relative outperformance.

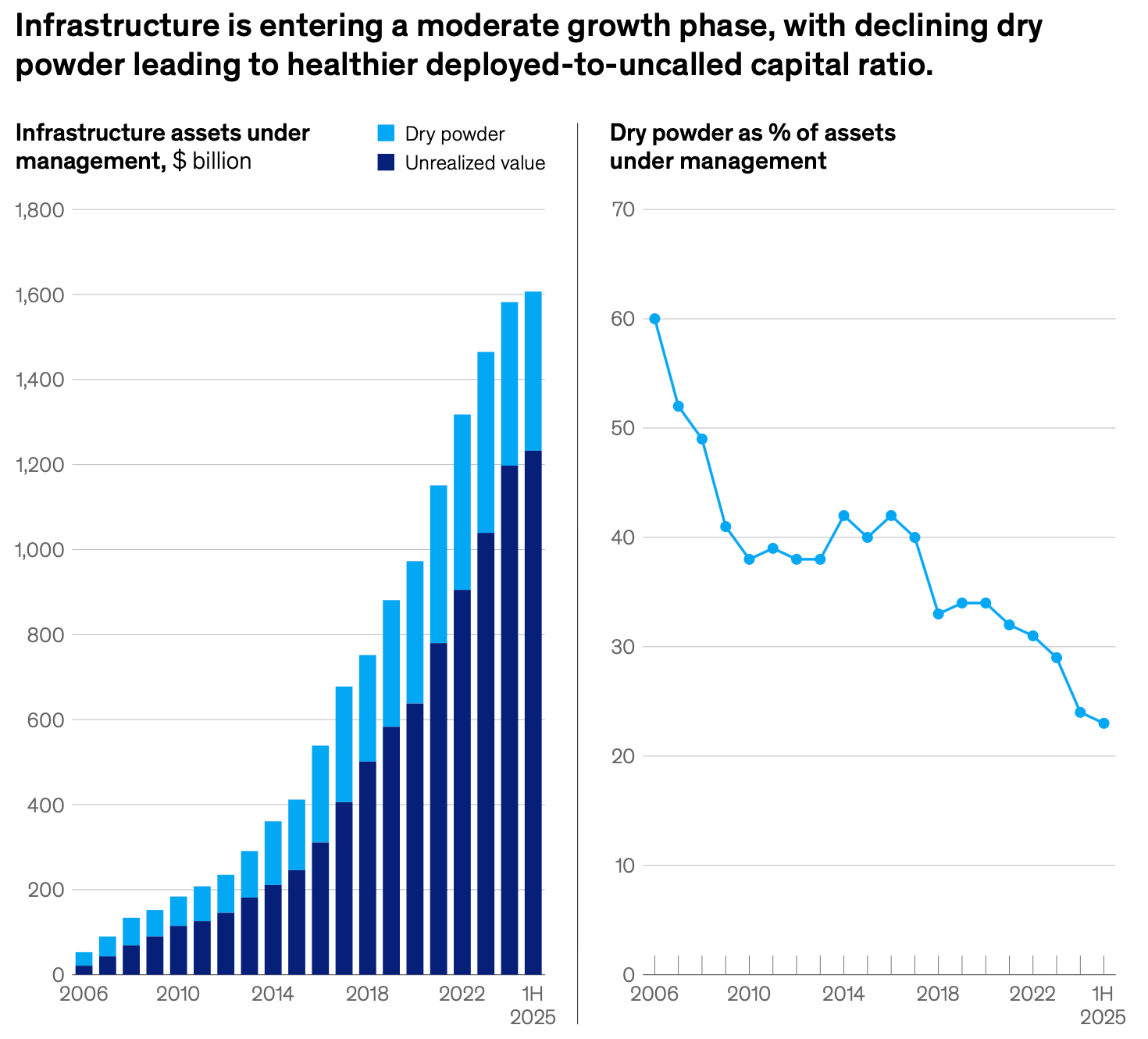

Infrastructure markets are showing greater maturity as excess capital declines and deployment improves. Historically, LP demand exceeded deal availability, leaving around 40 percent of assets under management unallocated between 2009 and 2017 due to a shortage of suitable opportunities. By mid-2025, this “dry powder” has fallen to about 23 percent of AUM, reflecting a better balance between fundraising and capital deployment.

At the same time, investment activity is shifting toward larger transactions. In 2025, total deal value increased by 23 percent despite a 24 percent drop in deal volume, while average deal sizes rose by 78 percent year over year. Liquidity is also strengthening, with secondary infrastructure funds expanding from one $5.3 billion vehicle to four funds totaling $4.3 billion. Collaboration between private and public investors is increasing, particularly in large scale projects such as fiber network expansion.

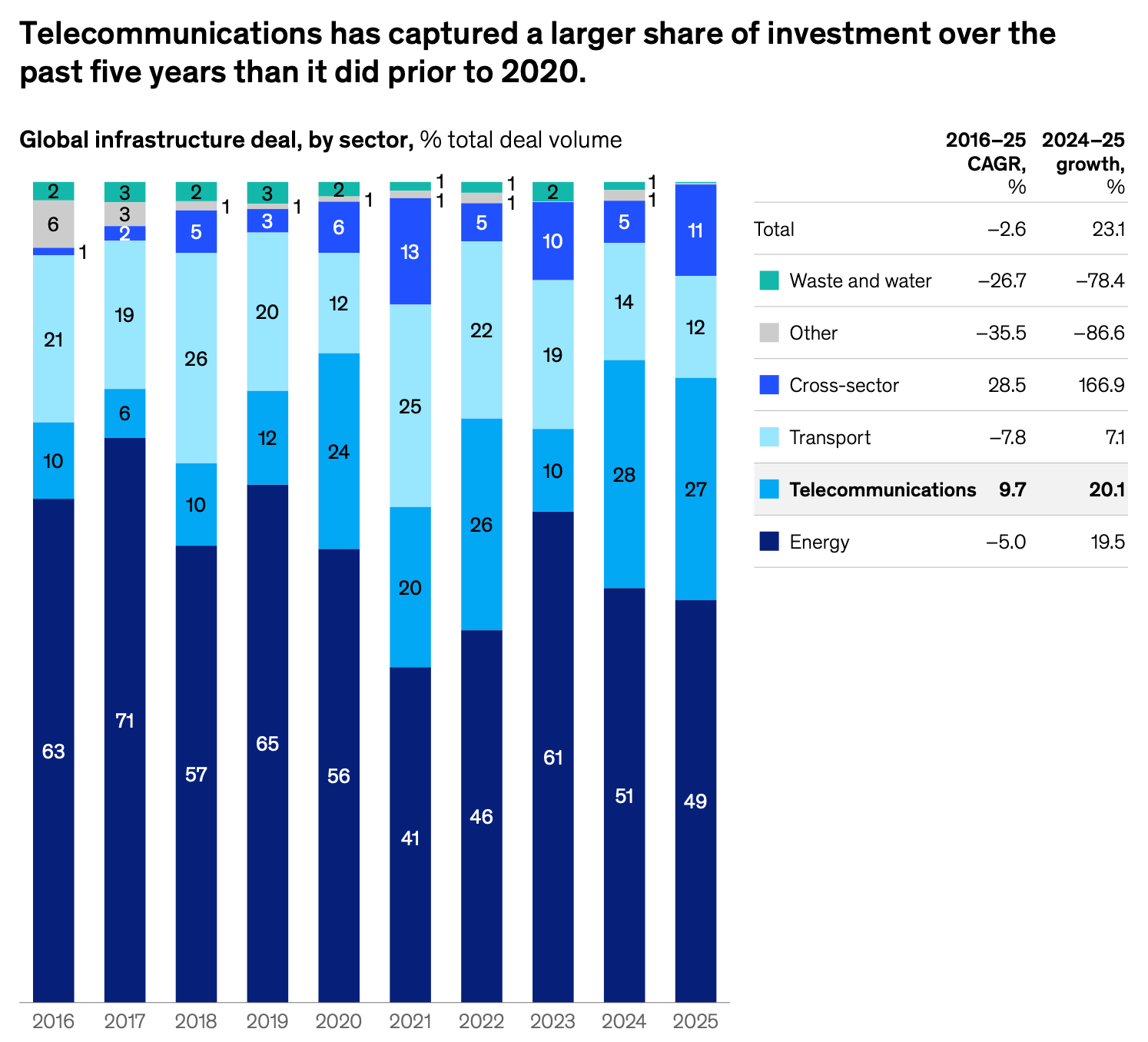

Infrastructure investment strategies are expanding beyond traditional assets into more complex and interconnected opportunities. Investors are moving up the risk spectrum and increasingly targeting areas where sectors converge, reflecting a broader definition of infrastructure.

New deal theses often combine energy, digital, and transport. Examples include data centers integrated with power infrastructure, electric vehicle networks supported by advanced connectivity, and waste management projects that produce sustainable aviation fuels. These cross sector models are becoming central to investment strategies.

As a result, capital is concentrating in larger, more diversified funds that can operate across multiple verticals and deploy capital flexibly. These platforms are generally better positioned to capture emerging opportunities and tend to outperform smaller peers, reinforcing a shift toward scale and integrated investment approaches in infrastructure markets.

Also, a couple of weeks ago I was at FIBE Berlin! It was an amazing event overall, with a lot of players from the fintech ecosystem! I also had the opportunity to interview Rabea Bader, co-founder of Quidkey, that you will find very soon on #Builders!

But let’s take a closer look at the main news of the last seven days. Revolut IPO could still be at least 2 years away according to Nik Storonsky, Visa and TikTok launch a creator focused debit card, Alipay supports now agentic payment through OpenClaw integration and Adyen acquired Talon.One for $750M. But also, Cash App released a parent managed kids account, Coinbase listed GBP linked stablecoin, American Express acquired Hyper and AC Milan renewed payment partnership with Corpay. In the VC ecosystem, Sideline Group closed a $155M fund, DFF Ventures launched a $70M fund III and Passion Capital a $40M fund IV. But also, Firstpoint VC, Homegrown Ventures and Robinhood Ventures. And finally, some very interesting funding rounds from fintech startups like Firenze, Monk, Takenos, Zenskar, Aro, Wealth.com and many others.

Let’s take a closer look:

Rounds

Wealth.com raises $65M Series B to scale AI driven wealth management platform

Zenskar raises $15m Series A for agentic B2B finance

Stripe alumni launch Seapoint with €7.5M to build AI native fintech platform

Salmon Group Ltd raises $100M to scale digital lending strategy in the Philippines

Nigeria government approves $75M investment in Flutterwave ahead of planned IPO

Firenze raises £6M to scale lombard lending infrastructure for wealth managers

Valstro launches next gen OMS with first client and $60M round

Monk raises $25M Series A to reinvent accounts receivable with AI

Takenos expands to Peru backed by $5M round to capture Latin America’s gig economy

Tencent takes strategic stake in Kaspi.kz with 6M ADS purchase

HATA raises $8M series A led by Bybit to expand Malaysia’s digital asset ecosystem

Aro secures $2.5M Pre-Seed to scale AI driven credit guidance in Brazil

BetHog 🐗 raises €8.5M to scale AI powered live dealer platform and launch B2B offering

Addi secures $150M credit facility led by J.P. Morgan and Fasanara Capital to scale BNPL growth in Colombia

Quillon (prev. Acclara AI) raises $1.5M to build audit grade AI for financial reporting

Astor (YC S25) raises $5M Seed to scale AI driven investment advisory platform

VC funds

Sideline Group closes a first $155M fund I

Homegrown Ventures closes a $22.8M fund I to back MENA consumer brands

DFF Ventures closes €70M Fund III as European pre seed momentum accelerates

Passion Capital closes £40M fund IV to back early stage AI and fintech founders

Firstpoint VC targets €50M fund to scale AI driven gaming across emerging markets

Robinhood Ventures Fund I invests $75M in OpenAI to expand retail access to private markets

News on the market

Revolut CEO Nik Storonsky says IPO is at least 2 years away

Payward to acquire Bitnomial in $550M deal, building fully regulated US crypto derivatives platform

American Express acquires Hyper to advance AI driven expense management

AC Milan and Corpay renew multi year FX partnership for cross borders payments

BVNK is now powering stablecoin payments for Meow

Revolut could be valued at $200B in the upcoming IPO

Lydian unveils Visa crypto card issued by Rain

Ramp Network launches multichain wallet to streamline self custody

Visa and TikTok launch UK ‘Creator Card’ to unlock faster income access

Nium partners with Coinbase to scale USDC payments across 190+ countries

HQLAᵡ secures strategic investment from Broadridge and digital asset to scale collateral mobility on canton

Revolut targets French and U.S. banking licences to speed up global expansion

Veem expands into stablecoins with USDV launch powered by Stripe’s Bridge

Cash App expands into gen alpha with parent managed accounts for kids

Alipay enables autonomous AI agent payments with OpenClaw integration

Adyen to acquire Talon.One for €750M to power real time commerce decisions

Coinbase lists tGBP as GBP stablecoins gain momentum in global payments

And here some useful resources for everyone involved in the ecosystem:

Events you don’t want to miss

Stablecon EMEA | Amsterdam - 19th-20th May (Link here)

Money 20/20 | Amsterdam - 02-04 June (Link here)

You have a cool event you want to mention or to sponsor? Feel free to send me a DM.

Founders to watch in fintech

I also wanted to start shining a light on the most interesting fintech founders out there, so I thought to start sharing how I look for ideas to invest on. Every week, I will start sharing the most interesting founders in fintech, divided per area.

This week we take a look at the most interesting founders in fintech in Turkey.

I usually use Spectre to scout for new ideas, the team is great and they also give me a free account once they learned I was a fan of the product. So if you wanna take a look at it, you can find it here.

New funds

I would like to leave this part of the newsletter as space for VC and solo GP that are launching new funds right now. I frequently speak with GPs and LPs, and I like the idea of giving them a showcase where to announce what they are doing. Here the new funds raising right now that I have been talking with:

Parallax Ventures, a fintech VC fund focused on Latam. They closed Fund I with a strong +50% IRR and 0.7x DPI, and are now raising Fund II. Take a look here if you want to know more or reach out directly to the GP at gennari@parallax.vc for details.

Founder Factor, VC focused on YC companies, that just closed investments on the latest YC W26. They are expanding the current vehicle to double down on the current batch. Partner is Marco Scotti, you can take a look here if you are interested.

Overall, very interesting to see where the VC ecosystem is heading recently, between new emerging managers, solo GP and micro funds.

Always happy to support if I can under this point of view! If you are raising a fund and you want to be listed here send me a message on Linkedin.

And finally, take also a look at the last edition of the newsletter, Weekly update #128.