Weekly update #125

The latest update from the fintech and VC ecosystem

Welcome to this edition of the weekly newsletter. The idea behind this is to gather all the information in the startup ecosystem in one place, with a special focus on the fintech market and the VC industry.

The last episode of Builders has been released this week! In this episode, I sit down with Michael Hurup Andersen, CEO and founder of kompasbank. You can find the full episodes here on YouTube, or here on Spotify and here on Apple Podcast and here on Amazon podcast, but take a quick look at a short clip from the video:

Michael is a Danish fintech entrepreneur and seasoned financial markets professional, currently serving as Founder and co-CEO of kompasbank, a Copenhagen based fintech focused on empowering small and midsized enterprises with integrated financial and operational solutions.

Coming from a Master’s degree in Finance from Aarhus University and Mathematical Finance at the University of Oxford, he has over two decades of experience across banking, trading, and advisory, he has held senior roles at institutions including Alvarez & Marsal, where he advised on M&A and private equity transactions, and Deloitte UK, where he led large teams in banking treasury and risk management.

Earlier in his career, he built deep expertise in capital markets at Saxo Bank and Nordea Markets, Corporates & Institutions, specializing in FX options, asset and liability management, and global macro strategies.

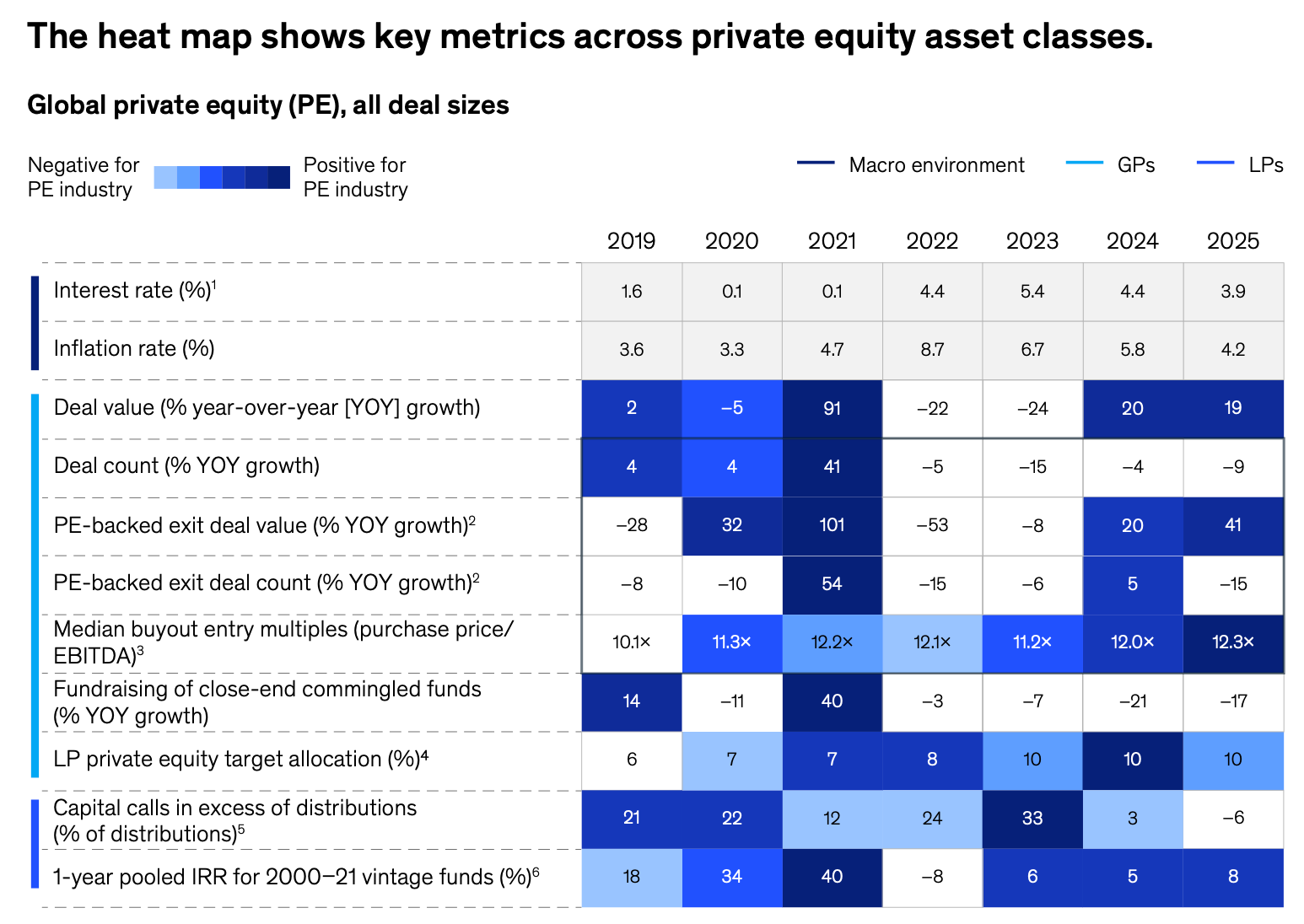

Coming back to us, this week I’ve been reading a very interesting report, the “Global private market reports 2026” by McKinsey & Company. The study is a very interesting overview of the last couple of years in private markets, including PE and VC, analysing deals value, exits, and dry powder from LP and GP. Here my main takeaways:

After three subdued years, private equity rebounded in 2025. Deals above $500 million rose 44 percent to over $1 trillion, a record, while total deal value increased 17 percent. Exits climbed more than 40 percent, with IPO-related exits nearly doubling. Megadeals above $2.5 billion returned, including the $55 billion take-private of Electronic Arts.

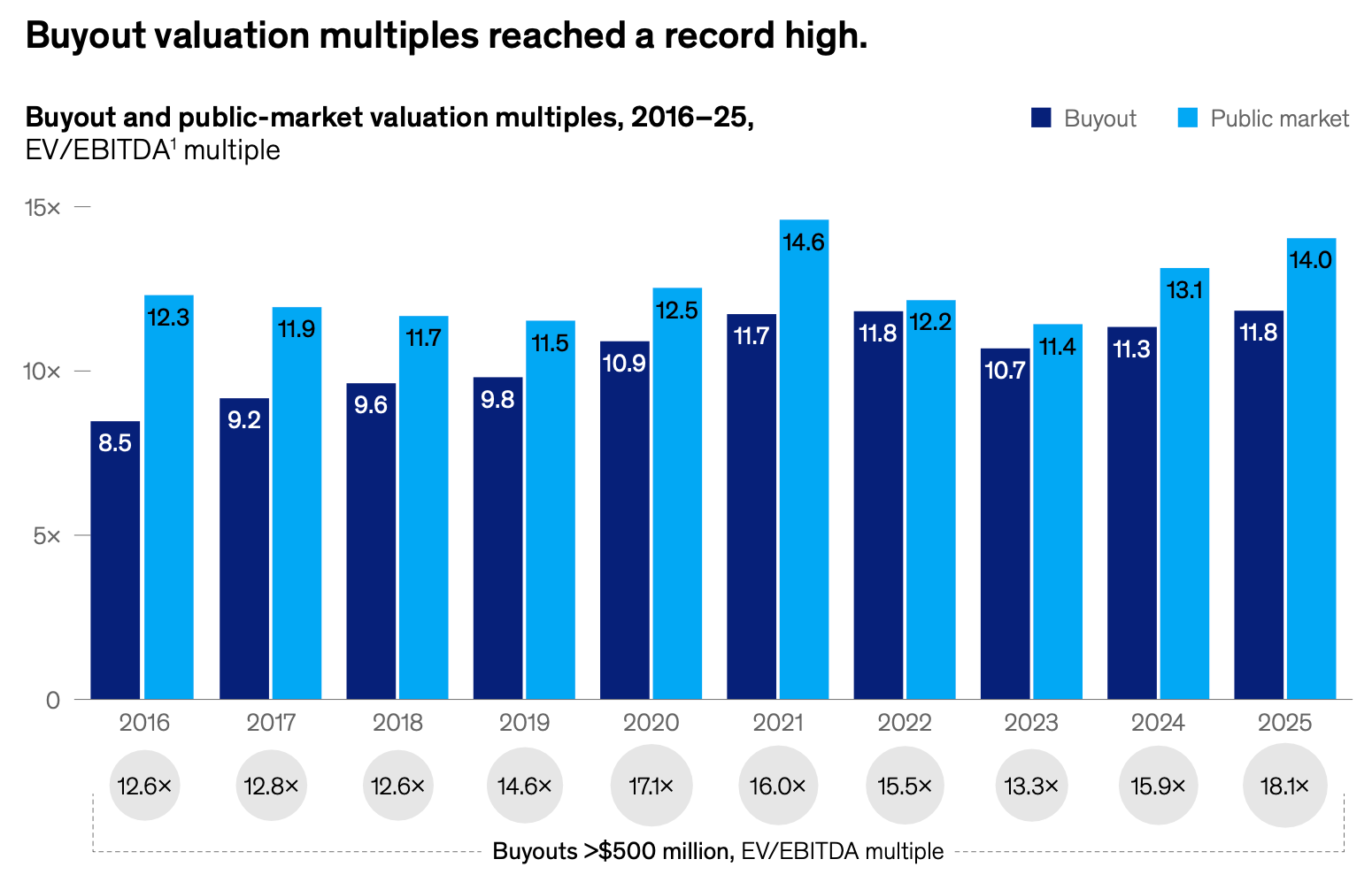

However, conditions remain demanding. Median purchase multiples rose from 11.3x to 11.8x EBITDA, while over 16,000 companies, or 52 percent of portfolios, are held beyond four years. Top-quartile returns reached 8 percent, versus 18 percent for the S&P 500 and 22 percent for the MSCI World, reinforcing a more competitive, structurally evolving market.

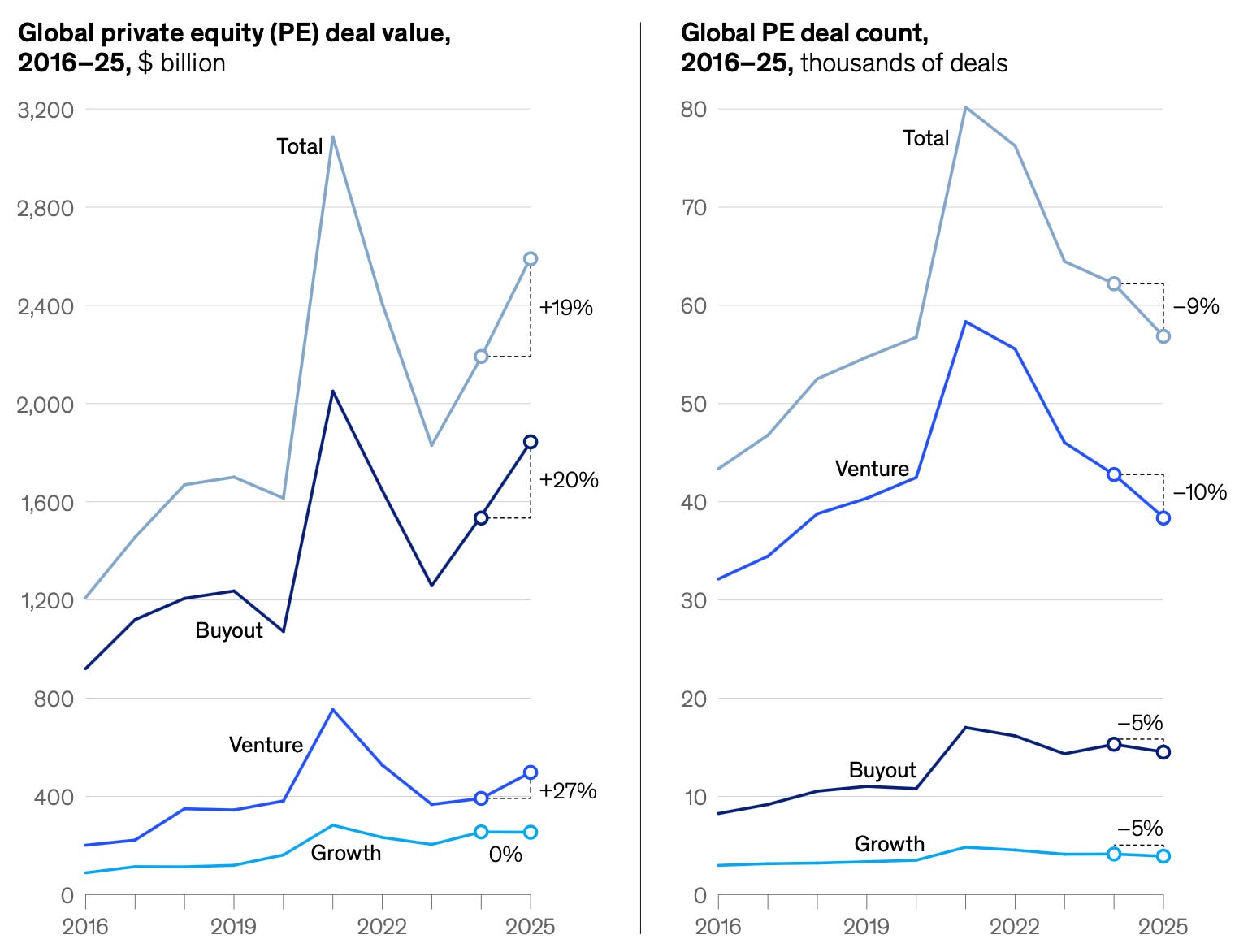

Private equity deal value rebounded in 2025, rising 19 percent to $2.6 trillion. Global buyout value reached nearly $1.8 trillion, up 20 percent and the second-highest on record, accounting for almost three-quarters of total growth.

Deals above $500 million increased 44 percent to $1.1 trillion. Large buyouts exceeded $900 billion, up 51 percent, while megadeals above $2.5 billion rose 72 percent to over $600 billion.

Despite this, total deal count fell 5 percent, though large deal volume grew 20 percent. Average buyout size surpassed $910 million, up from just over $610 million. Second-quarter value declined 13 percent, reflecting cautious execution.

Larger deals have returned as deployment pressure drives buyers to pay more for quality. The rise in deal value reflects higher pricing rather than increased volume, with median EBITDA multiples reaching a record 11.8x in 2025, slightly above 2022 levels.

This trend is partly driven by deal mix, as larger transactions command higher valuations due to stronger earnings stability. Over the past five years, deals above $500 million averaged 15.8x multiples, compared with 11.5x overall. Rising multiples also reflect scarce high-quality assets and sustained capital deployment pressure.

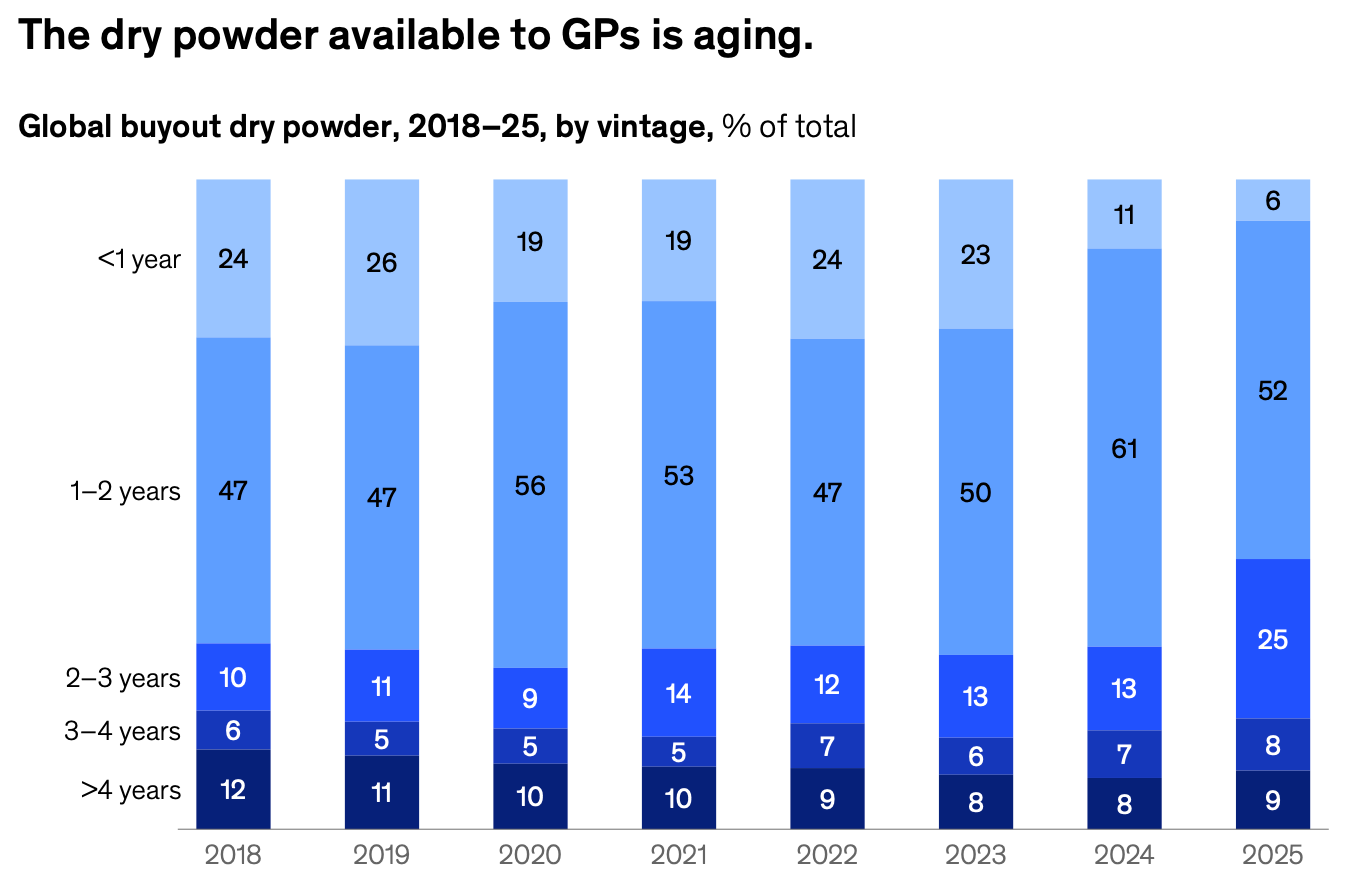

General partners are increasingly willing to pay more as aging dry powder builds. About 40 percent of capital was two years or older by June 2025, a new peak versus the past seven years. This pressure is driving higher equity deployment and greater pricing flexibility.

At the same time, limited supply of resilient assets is pushing a flight to quality, with premium multiples paid for stability. Larger buyouts are not matched by higher leverage, and equity contributions are rising. With leverage previously accounting for about 45 percent of returns between 2010 and 2022, operational value creation is becoming essential.

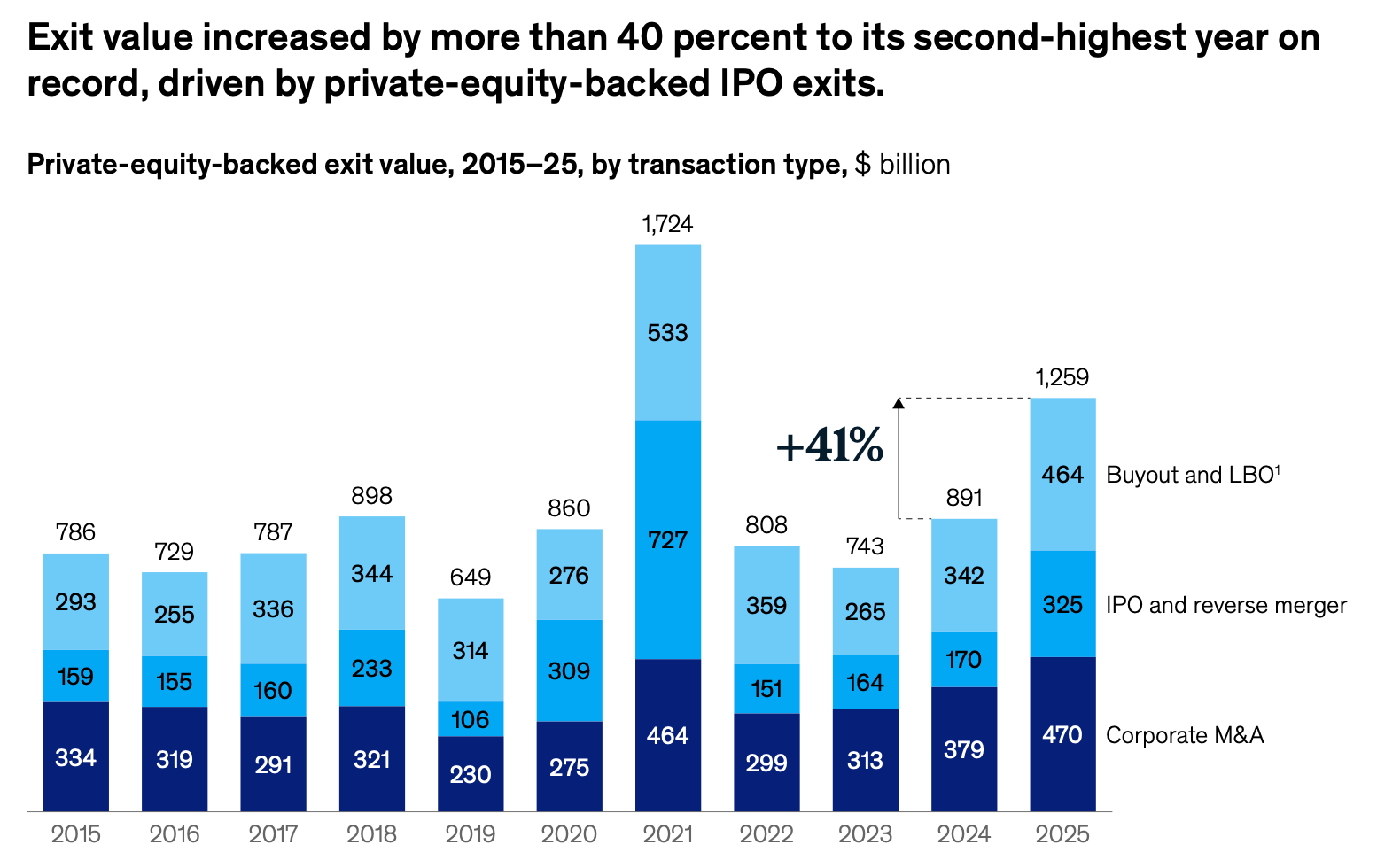

Exit value rebounded in 2025, rising 41 percent to $1.3 trillion, the second-highest on record. Growth was driven by PE-backed IPOs, which nearly doubled to over $320 billion, while total exit count fell 15 percent. IPO volumes increased 8 percent, unlike other exit types.

The 98 percent rise in IPO value was driven by deals above $2.5 billion, up 148 percent from $98 billion to $246 billion. IPOs represented 5 percent of exits by count but 23 percent of those above $500 million, reflecting stronger investor confidence and demand for large, high-quality assets.

But let’s take a closer look at the main news of the last seven days. Revolut posted their financial results for 2025, with $6B in revenue and $2.3B in profit, European Investment Fund (EIF) raised $15B fund of funds to back EU VCs, Coinbase launched bitcoin backed mortgages in partnership with Better, Kleiner Perkins raised $3.5B in new funds. But also, Visa Direct expands real time payment using Moonrise by Lunar, SumUp launches in app investing with Upvest, and Wero launches two new integrations with Nickel and Worldpay. Lots of news in the VC market! Air Street Capital raised a $232M fund, 360 Capital a $85M first close of their new $100M fund, and Cloudberry Ventures a $50M fund. But also new closing from Credo Ventures, Vitamin°C, BKR Capital, 5c(c) Capital and ParaFi Capital. And finally, some very interesting funding rounds from fintech startups like Theia Insights, Chexy, Spade, DOSS, Zalos (YC F25), Happy Pay, Eunice AI and many others.

Let’s take a closer look:

Rounds

Kalshi surpasses $1B raise at $22B valuation amid rapid growth and regulatory scrutiny

Talino Fintech Foundry raises $7.5M series A to build global fintech foundry for cross border payments

Happy Pay secures $5M seed led by Partech to scale interest free BNPL in South Africa

Zalos (YC F25) raises $3.6M seed to deploy AI agents across finance workflows

DOSS raises $55M Series B to bring AI native inventory into ERP ecosystems

Spade raises $40M series B to power AI driven payments intelligence

Worth AI secures $30M Series A to reinvent SMB onboarding and underwriting

littlefish secures $9.5M Series A to build merchant infrastructure across Africa

Glimpse raises $35M Series A to automate retail finance disputes with AI

Finfinity raises $2.4M to scale digital lending marketplace in India

Eunice AI raises $8M to build AI infrastructure for institutional due diligence

Subbyx raises €30M Series A to expand subscription infrastructure across Europe

Theia Insights raises $8M to build AI powered map of global financial markets

Chexy raises CAD $14M series A to expand rewards driven payments platform

Prestamype secures $27M to scale SME lending and launch investment platform

VC funds

Air Street Capital raises $232M fund III to scale AI first innovation across Europe and North America

360 Capital secures €85M first close for Poli360 2 deeptech fund, targets €100M

Cloudberry Ventures launches €50M deeptech fund to tackle AI infrastructure constraints

Credo Ventures raises $88M Fund 5 to back pre seed founders across EU

Vitamin°C launches €18M climate fund targeting early stage impact amid VC slowdown

Kleiner Perkins raises $3.5B in new funds to double down on AI investments

BKR Capital raises $14.5M toward $50M Fund II to back black founders

Kalshi and Polymarket CEOs back $35M prediction markets fund by 5c(c) Capital

ParaFi Capital raises $125M venture fund to double down on institutional crypto

European Investment Fund (EIF) is raising €15B fund of funds to unblock €80B for EU startups

News on the market

Coinbase introduces stock perpetual futures, expanding 24/7 access to US equities

Grab to acquire foodpanda Taiwan for $600M, expanding beyond Southeast Asia

Revolut posts financial results for 2025, with $2.3B profit and $6B in revenues

Worldpay (now Global Payments Inc.) integrates Wero to expand pan European instant payments acceptance

Miro acquires Reforge to strengthen AI driven product innovation

Venmo expands globally with PayPal integration across 90 Markets

Nubank eyes $10M per year stadium naming deal with S.E. Palmeiras

Paysend integrates stablecoins via BVNK to accelerate cross border payments

SumUp launches in app investing for merchants through Upvest partnership

Nickel integrates Wero to accelerate Europe’s push for sovereign payments

Plaid acquires This Week in Fintech to expand Its ecosystem reach

Coinbase and Better launch crypto backed mortgages for homebuyers

And here some useful resources for everyone involved in the ecosystem:

Events you don’t want to miss

FIBE | Berlin - 15th-16th April 2026 (Link here)

Stablecon EMEA | Amsterdam - 19th-20th May (Link here)

You have a cool event you want to mention or to sponsor? Feel free to send me a DM.

Founders to watch in fintech

I also wanted to start shining a light on the most interesting fintech founders out there, so I thought to start sharing how I look for ideas to invest on. Every week, I will start sharing the most interesting founders in fintech, divided per area.

This week we take a look at the most interesting founders in fintech, in France.

I usually use Spectre to scout for new ideas, the team is great and they also give me a free account once they learned I was a fan of the product. So if you wanna take a look at it, you can find it here.

New funds

I recently spoke with Marco Scotti from Raspberry Ventures. Thanks to their Y Combinator Alumni network, they unlock access to the top 10% of YC companies for Angel investors. Co-investing up to $3M across 15 - 25 companies in each YC batch, 4 batches a year, before Demo Day; and before the Silicon Valley VCs come in and take allocations in the best companies.

Their next batch YC W26m is closing in the upcoming weeks. You can take a look here if you are interested!

Take also a look at the last edition of the newsletter, Weekly update #124.