Weekly update #121

The latest news from the fintech and VC ecosystem

Welcome to this edition of the weekly newsletter. The idea behind this is to gather all the information in the startup ecosystem in one place, with a special focus on the fintech market and the VC industry.

The latest episode of Builders has been released this week! In this episode, I sit down with Lucrezia Lucotti, partner at 360 Capital. You can find the full episodes here on YouTube, or here on Spotify and here on Apple Podcast.

Lucrezia Lucotti is Partner at 360 Capital, where she focuses on Italian and Southern European dealflow across B2B and B2C software, deeptech and climate tech ventures. She oversees investments and portfolio management across the firm’s 360 Deeptech, Climate Tech and Series A funds, following a progression from Analyst to Investment Director before being appointed Partner in January 2024.

Over the past five years at 360 Capital, Lucrezia has built a strong track record in sourcing, executing and managing early and growth stage investments. Prior to venture capital, she worked at Roland Berger as a Business Analyst on due diligences and industrial plans across financial services, pharma and industrial machinery, and gained experience at Gartner and Accenture in consulting roles spanning TMT and financial services, including the design of a new internet banking experience for SMEs

A Bocconi graduate with a double degree from WU Vienna, Lucrezia combines analytical rigor with a deep interest in innovation and entrepreneurship, and has also served as Ambassador for Female Founders, supporting the next generation of European entrepreneurs.

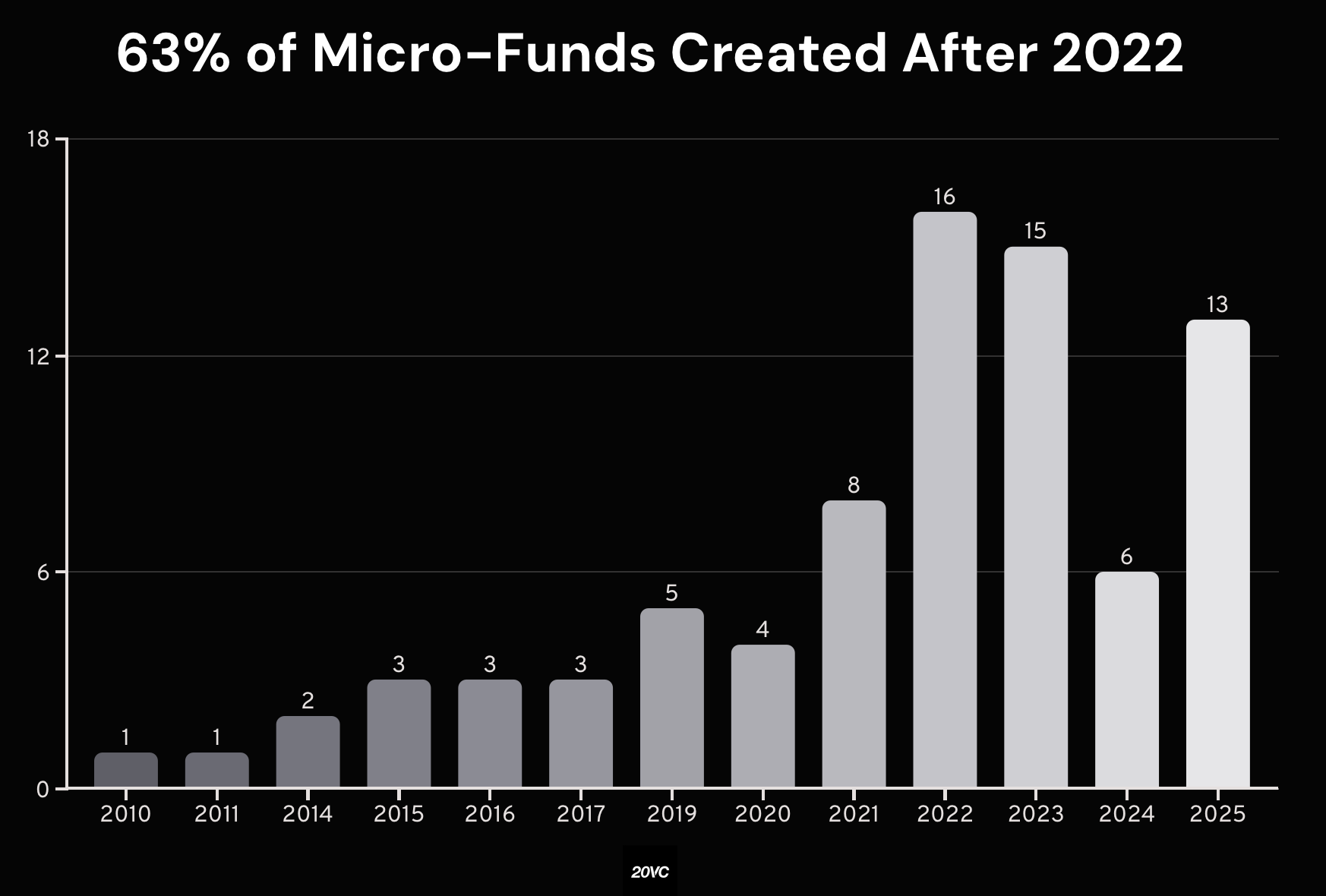

Coming back to us, this week I’ve been reading a very interesting report, the “State of European Micro-funds” by 20VC . The study, is a very interesting overview of the micro-funds trend in Europe in the last couple of years, with a full analysis of the scope, the size and the impact of this activity, including main emerging managers in the continent. Here my main takeaways:

According to the data, 63 percent of micro funds were launched after 2022, with 16 new vehicles in 2022, 15 in 2023, and 13 in 2025 alone. This compares with much lower annual figures throughout the 2010s, when launches typically ranged between one and five per year. The surge reflects a structural shift in the European venture landscape, with smaller, specialized managers emerging to address early stage capital gaps and more focused sector strategies.

While 41 percent of vehicles are led by solo GPs, the majority, 59 percent, are managed by teams, suggesting a growing preference for shared decision making and broader sourcing capacity. Geographically, 64 percent operate with a pan European mandate, compared to 36 percent that remain country focused, reflecting ambition to capture cross border opportunities.

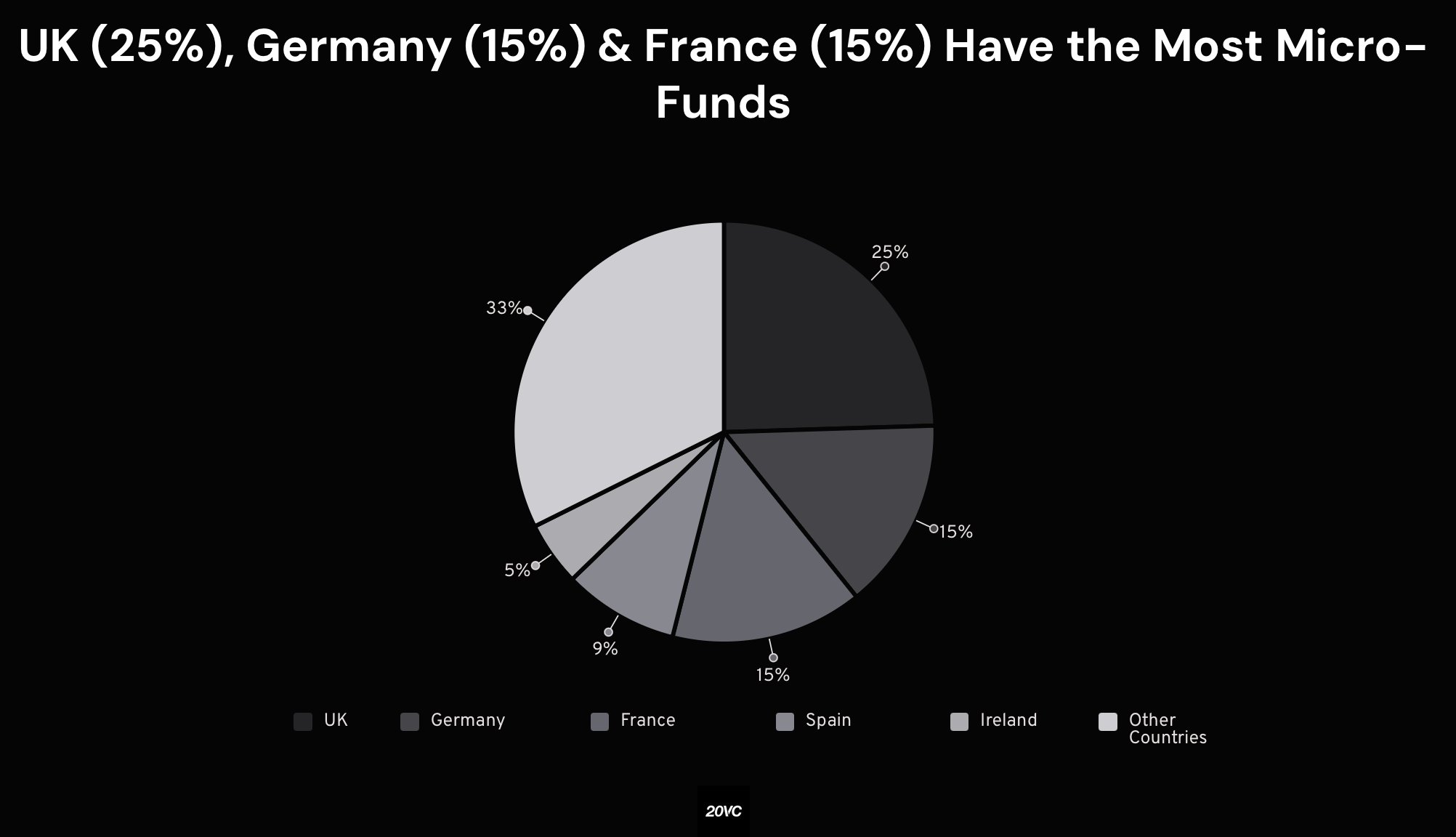

The UK accounts for 25 percent of micro funds, followed by Germany and France at 15 percent each, while Spain represents 9 percent and Ireland 5 percent. The remaining 33 percent is distributed across other European markets, indicating a widening footprint beyond traditional hubs. Together, the data points to a maturing segment combining concentrated national strength with an increasingly continental investment scope.

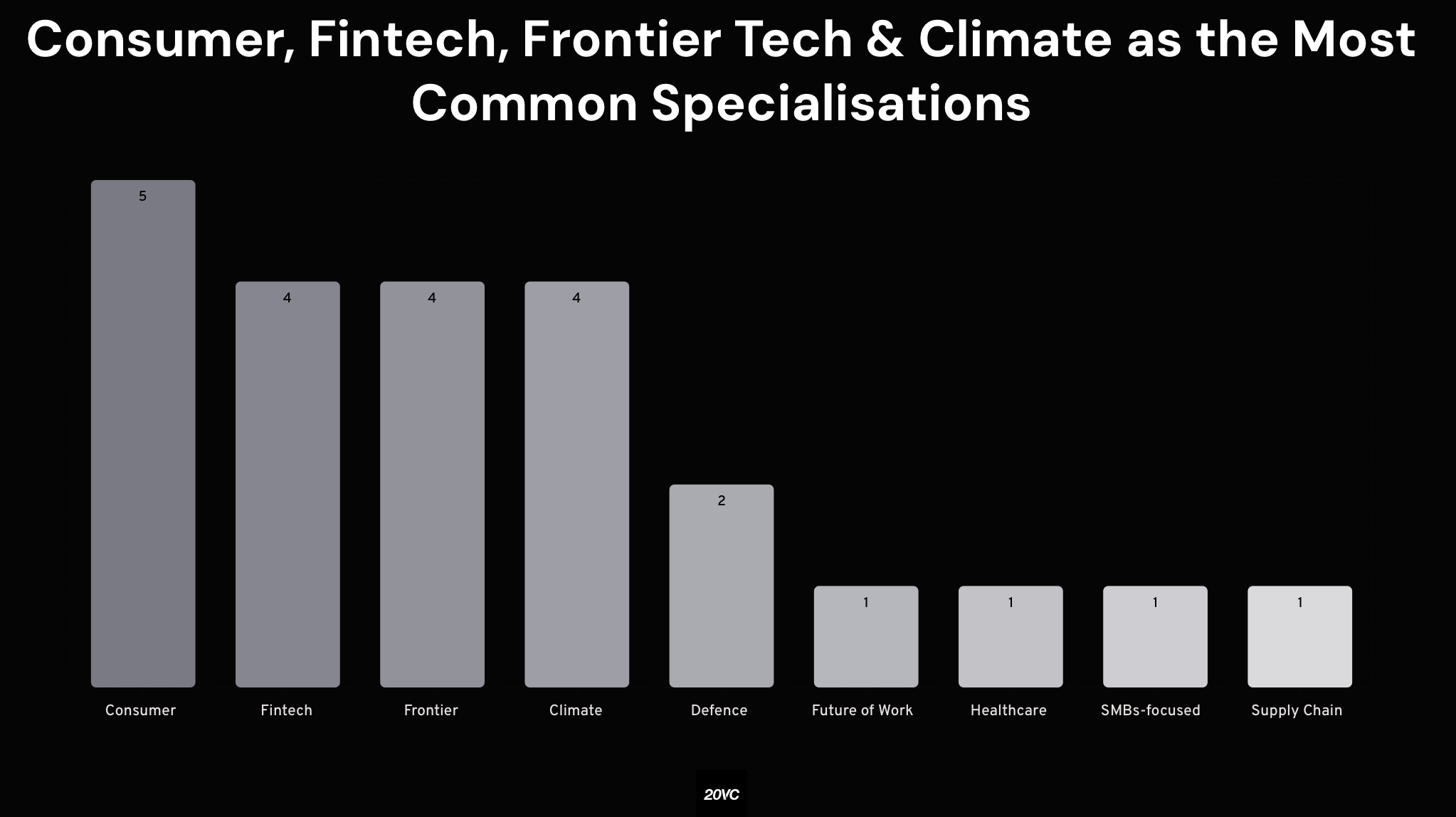

The study indicates that most European micro funds maintain a broad investment approach, with 71 percent operating as generalists and 29 percent pursuing a thematic strategy. Among specialist managers, the most common areas of focus are consumer, fintech, frontier technology and climate. Consumer leads with five dedicated funds, while fintech, frontier tech and climate each account for four.

Defence appears with two focused vehicles, and future of work, healthcare, SMBs and supply chain register more limited representation with one fund each. The data suggests that while sector specialization is present and often aligned with structural trends such as digital finance and climate transition, the prevailing model in the micro fund segment remains diversified, allowing managers to remain flexible across stages and verticals in a still evolving European venture landscape.

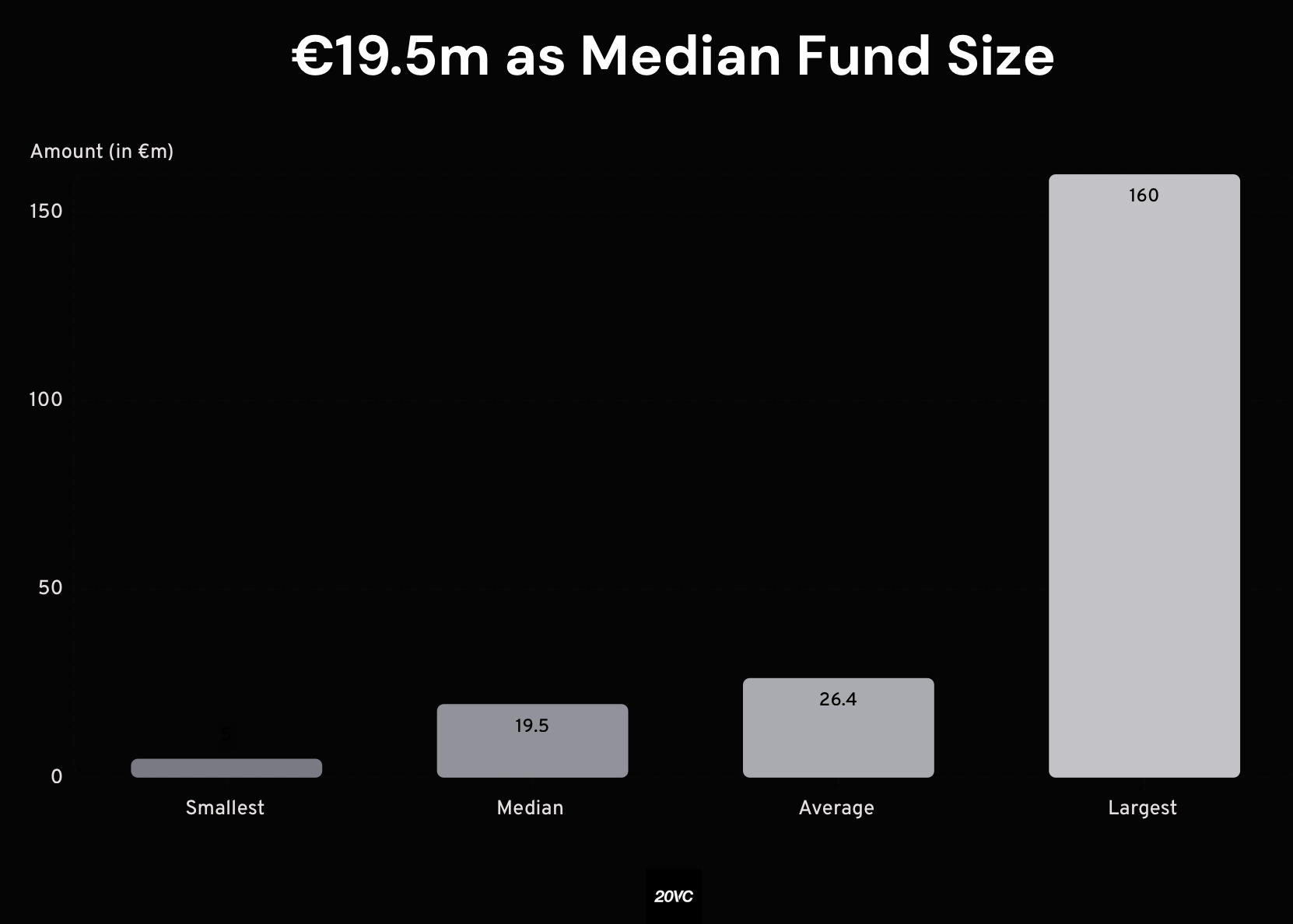

The study also shows a median fund size of €19.5 million among European micro funds, with an average of €26.4 million, indicating a right skew driven by a limited number of larger vehicles. The smallest fund stands at €5 million, while the largest reaches €160 million, illustrating the breadth within the segment despite its micro fund label.

On deployment, the median initial check size is €300,000, compared to an average of €440,000, again reflecting dispersion across strategies. The smallest reported ticket is €10,000 and the largest €2.6 million. Overall, the data suggests that European micro funds are structured to operate at a true early stage, writing relatively small initial checks while preserving capital for follow on, yet with flexibility to scale commitments when conviction and opportunity justify it.

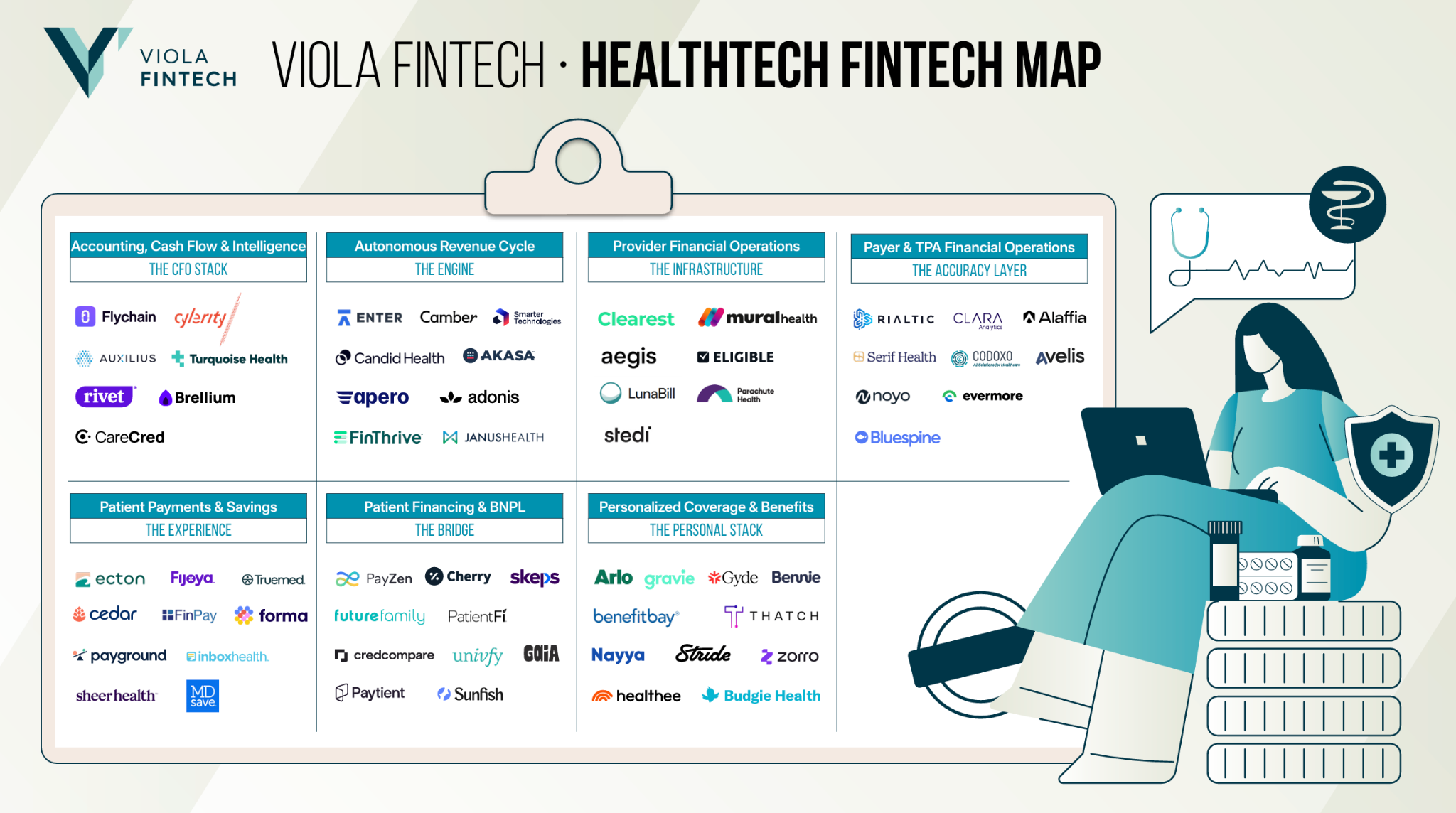

I’ve also read another interesting report this week, the “Healthtech fintech map” from Viola FinTech. A very comprehensive overview of the healthtech fintech ecosystem globally, a market that spans from CFO and cash flow tools, to autonomous revenue cycle platforms, provider and payer financial operations, patient payments and financing, and personalized coverage solutions. The breadth of companies across accounting, BNPL, benefits optimization and reimbursement accuracy reflects increasing digitization of healthcare economics.

But let’s take a closer look at the main news of the last seven days. Meta explores stablecoins payments integration, Crypto.com secures conditional approval for US banking license, Revolut is doing a secondary sale at $100B valuation, and Stripe is considering a PayPal acquisition. But also, Checkout.com returns to profitability, Coinbase launches stocks trading in the US and Apple eyes mid 2026 to launch payments services in India. Lots of new funds this week, Peak XV Partners closes $1.3B fund to focus on India, Seraphim Space space a $84M new fund for a spacetech fund, but also Syndicate One and Guinness Ventures with new funds. And finally, some very interesting funding rounds from fintech startups like Rhythmic, Inscope, WafR, Xflow, Secfix, Plaid, Basis and many others.

Let’s take a closer look:

Rounds

Former American Express and Mastercard executives raise $4M to mainstream stablecoins with Rhythmic

EFEX raises $8M seed to scale cross border treasury between Mexico and the U.S.

Inscope secures $14.5M Series A to modernize financial reporting with AI

Roopya secures ₹4 Crore seed round to scale AI powered lending infrastructure

Wayflyer surpasses $100M revenue, secures $250M credit facility to scale SMB lending

Stripe and PayPal Ventures back Xflow in $16.6M round to modernize India’s cross border B2B payments

Pantera Capital leads $11.5M Series A in hyperliquid superApp Based

Sherpas raises $3.2M seed to build AI native infrastructure for wealth managers

WafR raises $4M seed to scale last mile fintech infrastructure in Morocco

Basis becomes a unicorn with $100M round to automate accounting workflows

Dytto raises €1.5M to Bring AI Into Accountants’ Daily Workflow

Thema secures $6.2M to scale AI infrastructure for portfolio expansion

BCP injects €90M into ActivoBank as digital arm scales rapidly

Hypercore raises $13.5M series A to modernise private credit operations with AI

Secfix raises $12M Series A to reduce compliance work by 90%

Tether.io invests $200M in Whop at $1.6B valuation to power stablecoin creator economy

Alpa raises $3.5M pre seed to bring real time financial visibility to hospitality

Finrob raises $3.9M to scale AI native research for crypto and financial markets

Singapore’s Lyte secures $4.2M to expand financial tools for independent workers

Platinum Credit Uganda Limited secures $4M from Symbiotics to expand SMEs and household lending

t54 Labs raises $5M seed to build trust infrastructure for the agentic economy

Croissant secures $28M to repay brands and scale resale driven commerce

STS Digital Ltd secures $30M to scale institutional crypto options platform

VC funds

Syndicate One closes €22M second fund to scale Belgian tech globally

Guinness Ventures launches £3M SEIS fund to back early stage UK founders

Peak XV Partners raises $1.3B to deepen AI and India focus amid intensifying VC competition

Seraphim Space closes a €84M fund as European spacetech momentum builds

News on the market

Stripe valuation jumps to $159B in tender offer as volume reaches $1.9T

Checkout.com returns to profitability as volume surpasses $300B in 2025

Meta explores stablecoin payments integration, taps Stripe and other providers with an RFP

Canaan Inc. acquires Cipher Digital stake in $40M West Texas Bitcoin deal

Crypto.com secures conditional approval for US national trust bank charter

Stripe is reported considering a possible PayPal acquisition!

Revolut targets $100B valuation in secondary share sale and $150B IPO

Coinbase launches commission free stock trading for US users

Telegram Messenger emerges as fastest growing fraud channel in 2025 in Consumer Security report from Revolut

Verdane to acquire Augmentum Fintech in £185.7m Deal

And here some useful resources for everyone involved in the ecosystem:

Events you don’t want to miss

FIBE | Berlin - 15th-16th April 2026 (Link here)

Stablecon EMEA | Amsterdam - 19th-20th May (Link here)

You have a cool event you want to mention or to sponsor? Feel free to send me a DM.

Founders to watch in fintech

I also wanted to start shining a light on the most interesting fintech founders out there, so I thought to start sharing how I look for ideas to invest on. Every week, I will start sharing the most interesting founders in fintech, divided per area.

This week we take a look at the most interesting founders in fintech in Sweden.

I usually use Spectre to scout for new ideas, the team is great and they also give me a free account once they learned I was a fan of the product. So if you wanna take a look at it, you can find it here.

New funds

I recently spoke with Marco Scotti from Raspberry Ventures. Thanks to their Y Combinator Alumni network, they unlock access to the top 10% of YC companies for Angel investors. Co-investing up to $3M across 15 - 25 companies in each YC batch, 4 batches a year, before Demo Day; and before the Silicon Valley VCs come in and take allocations in the best companies.

Their next batch YC W26m is closing in the upcoming weeks. You can take a look here if you are interested!

Take also a look at the last edition of the newsletter, Weekly update #120.