Weekly update #116

The latest news from the fintech and VC ecosystem

Welcome to this edition of the weekly newsletter. The idea behind this is to gather all the information in the startup ecosystem in one place, with a special focus on the fintech market and the VC industry.

Builders is back! The latest episode was released last week! In this one, I sit down with Sir Gabriel Holbach, partner and CPO at 0TO9 | Bank of Entrepreneurship. You can find the full episodes here on YouTube, or here on Spotify and here on Apple Podcast.

Sir Gabriel Holbach is Partner & Chief Product Officer at 0TO9, where he helps founders turn early-stage ideas into scalable, user-centered fintech products. With over 13 years of experience in product design, UX strategy, and digital brand development across fintech, healthtech, and SaaS, he combines creative vision with operational precision.

Before joining 0TO9, Gabriel co-founded Penta (today Qonto ), one of Europe’s leading SME-focused digital banks, where he led product design from MVP to 50,000+ users. He built and scaled design teams, managed agile squads, and developed a cohesive user journey from onboarding to dashboard through a reusable design system. Later, at Index Health, he led UX strategy and design systems, improving product–market fit to 68% and reducing customer acquisition costs by 66%.

0TO9 is a fintech venture builder and investor aiming to launch 1,000 profitable European fintechs by 2045. Founded in Sweden in 2025, the company provides entrepreneurs with capital, compliance, talent, technical, and operational support needed to start and scale licensed financial companies in months rather than years.

Coming back to us, this week I’ve been reading a very interesting report from Alexandre Dewez of 20VC this week, the “States of French ecosystem in 2025”. The report is an overview on the startup ecosystem in France in terms of investments, number of deals, main trends, with a strong comparison on 2024 and the years before, trying to paint a picture of the status of the entire ecosystem. Here my main takeaways:

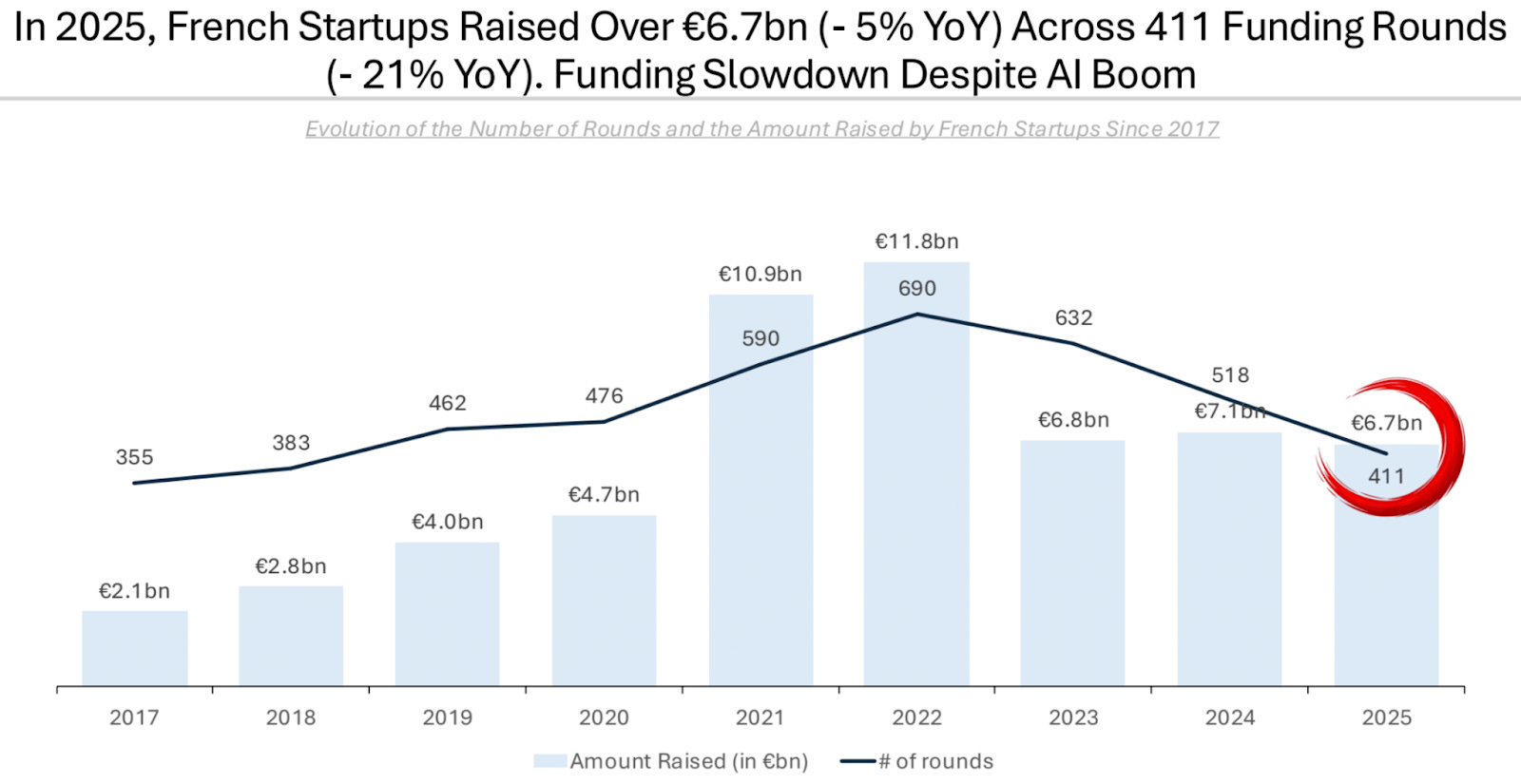

There is a sign of a clear cooling in VC investments in the French startup ecosystem in 2025. French startups raised €6.7bn across 411 funding rounds, marking a 5% year-on-year decline in capital deployed and a sharper 21% drop in deal count. This follows a peak in 2022, when funding reached €11.8bn across 690 rounds, and a strong 2021 at €10.9bn and 590 rounds. Despite sustained interest in AI, overall activity has continued to contract from 2023 (€6.8bn, 632 rounds) and 2024 (€7.1bn, 518 rounds), signalling a more selective VC environment.

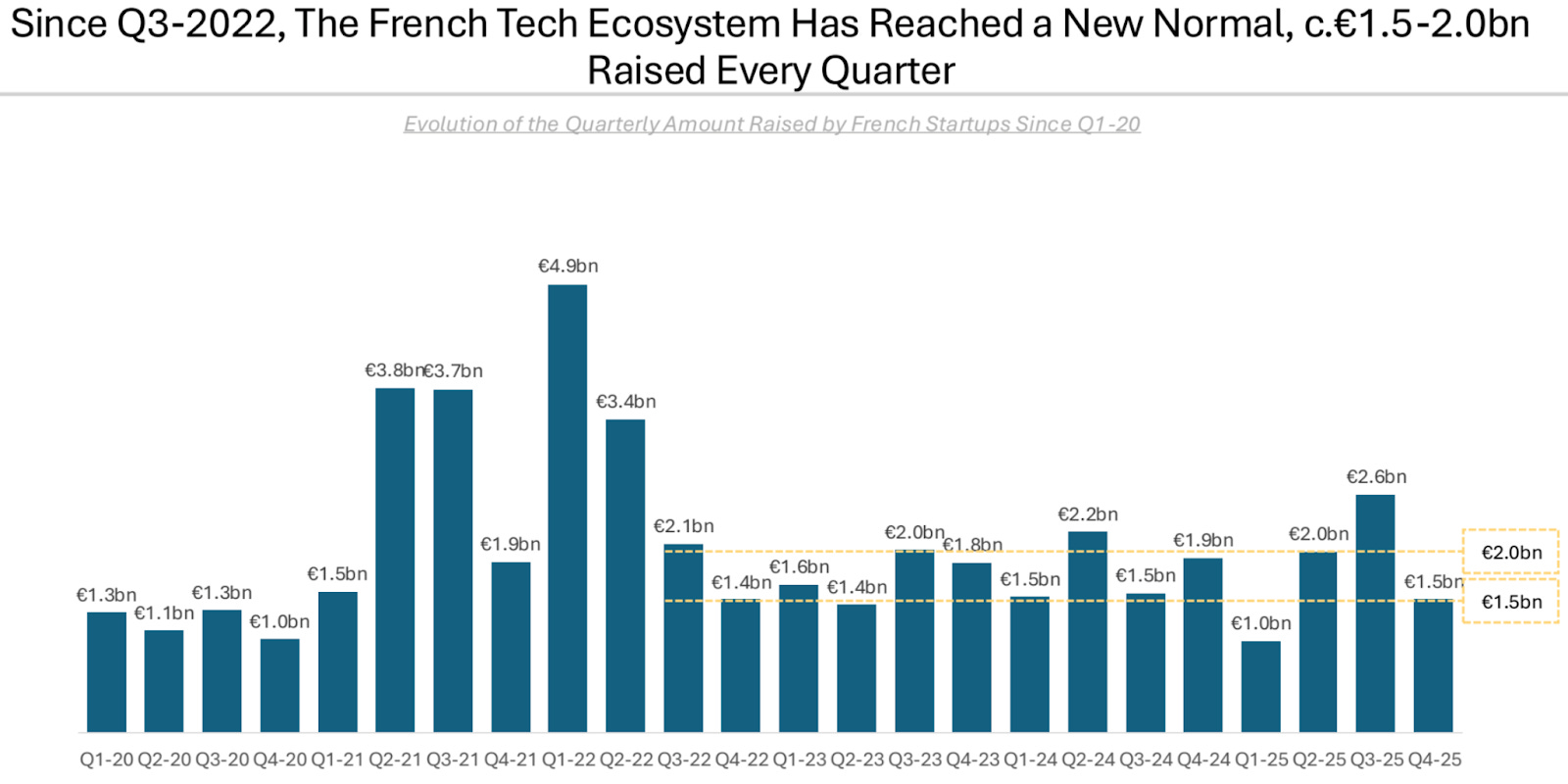

After record quarters in 2021 and early 2022, including a €4.9bn peak in Q1 2022 and €3.4bn in Q2 2022, quarterly funding has stabilized within a narrower €1.5–2.0bn range. From Q3 2022 through Q4 2025, most quarters consistently fall within this band, with limited upside such as €2.2bn in Q2 2024 and €2.6bn in Q3 2025. This pattern suggests a new, more disciplined VC environment, marked by lower volatility and sustained but selective capital deployment.

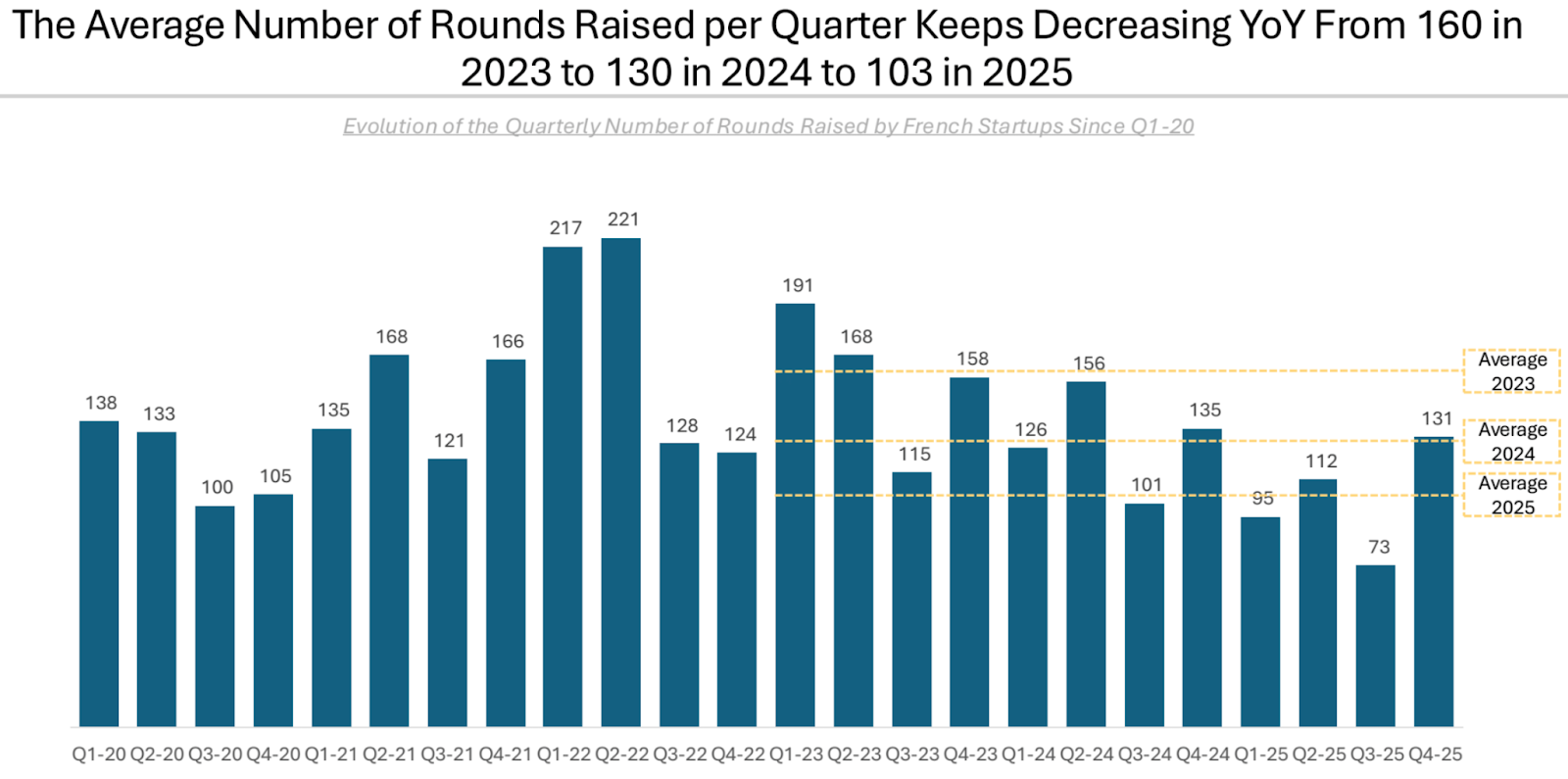

The average number of funding rounds per quarter declined from 160 in 2023 to 130 in 2024, reaching 103 in 2025. After peaking in early 2022 with over 220 rounds per quarter, activity steadily weakened, with notable lows such as 95 rounds in Q4 2024 and just 73 rounds in Q2 2025. Despite occasional rebounds, including 131 rounds in Q4 2025, the overall trend points to fewer transactions, reflecting increased selectivity among investors and a continued tightening of venture capital deployment.

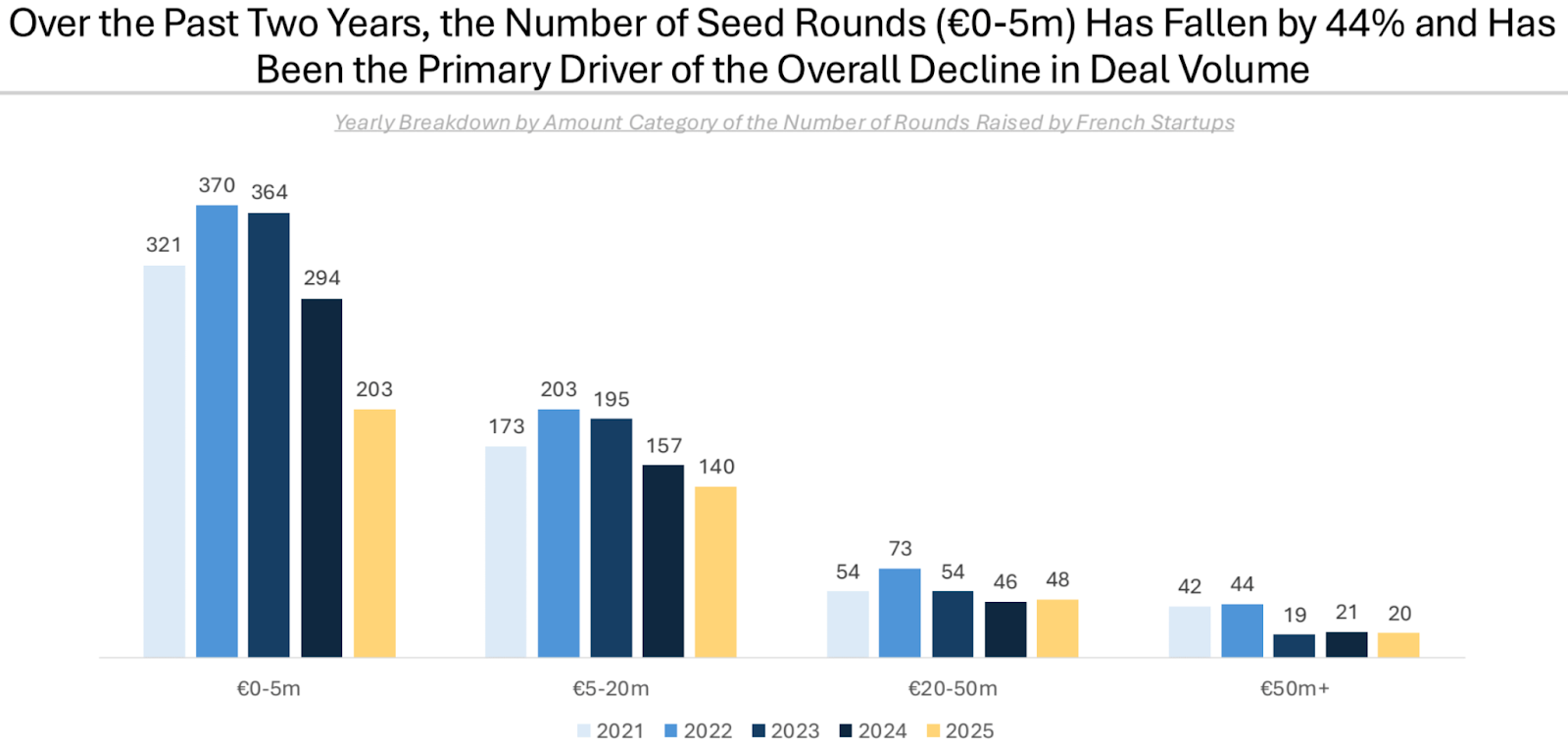

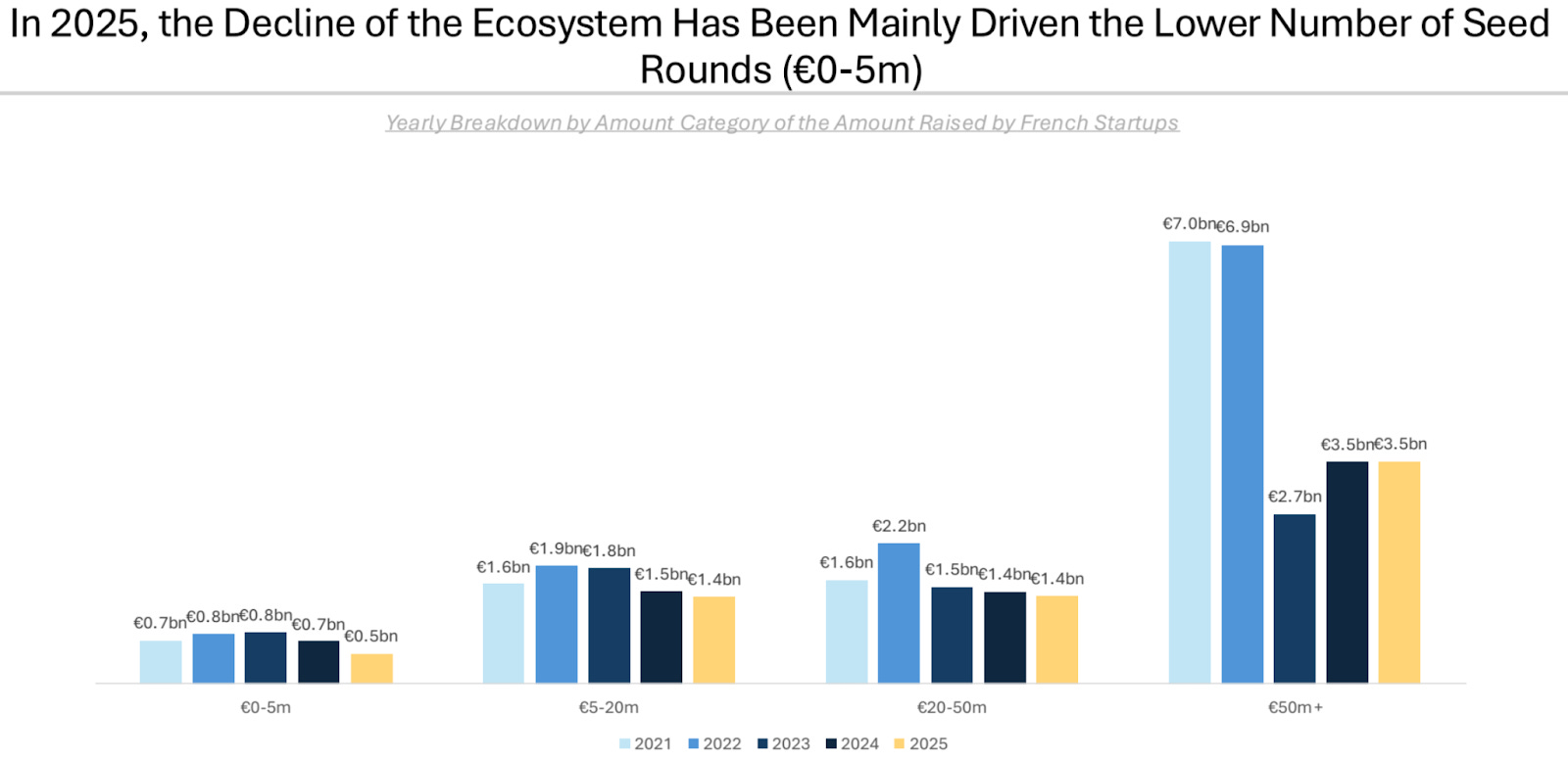

The decline in VC deal activity in France has been primarily driven by a sharp contraction in seed-stage funding. The number of €0–5m rounds fell from 364 in 2023 to 203 in 2025, a 44% drop in two years. Mid-stage rounds of €5–20m also declined, from 195 in 2023 to 140 in 2025, while larger rounds proved more resilient. Deals of €20–50m slipped from 54 to 48, and €50m+ rounds edged down from 19 to 20. This indicates that early-stage capital scarcity is the main factor behind the reduced overall deal volume.

The 2025 slowdown in VC investments in France is also largely attributable to weaker seed-stage funding. Capital raised in €0–5m rounds declined to €0.5bn in 2025, down from €0.7bn in 2024 and €0.8bn in both 2022 and 2023. Mid-stage funding remained relatively stable, with €5–20m rounds at €1.4bn and €20–50m rounds at €1.4bn in 2025. In contrast, large rounds proved resilient, with €50m+ deals reaching €3.5bn, unchanged year on year. This confirms that early-stage contraction, rather than late-stage weakness, drove the overall decline.

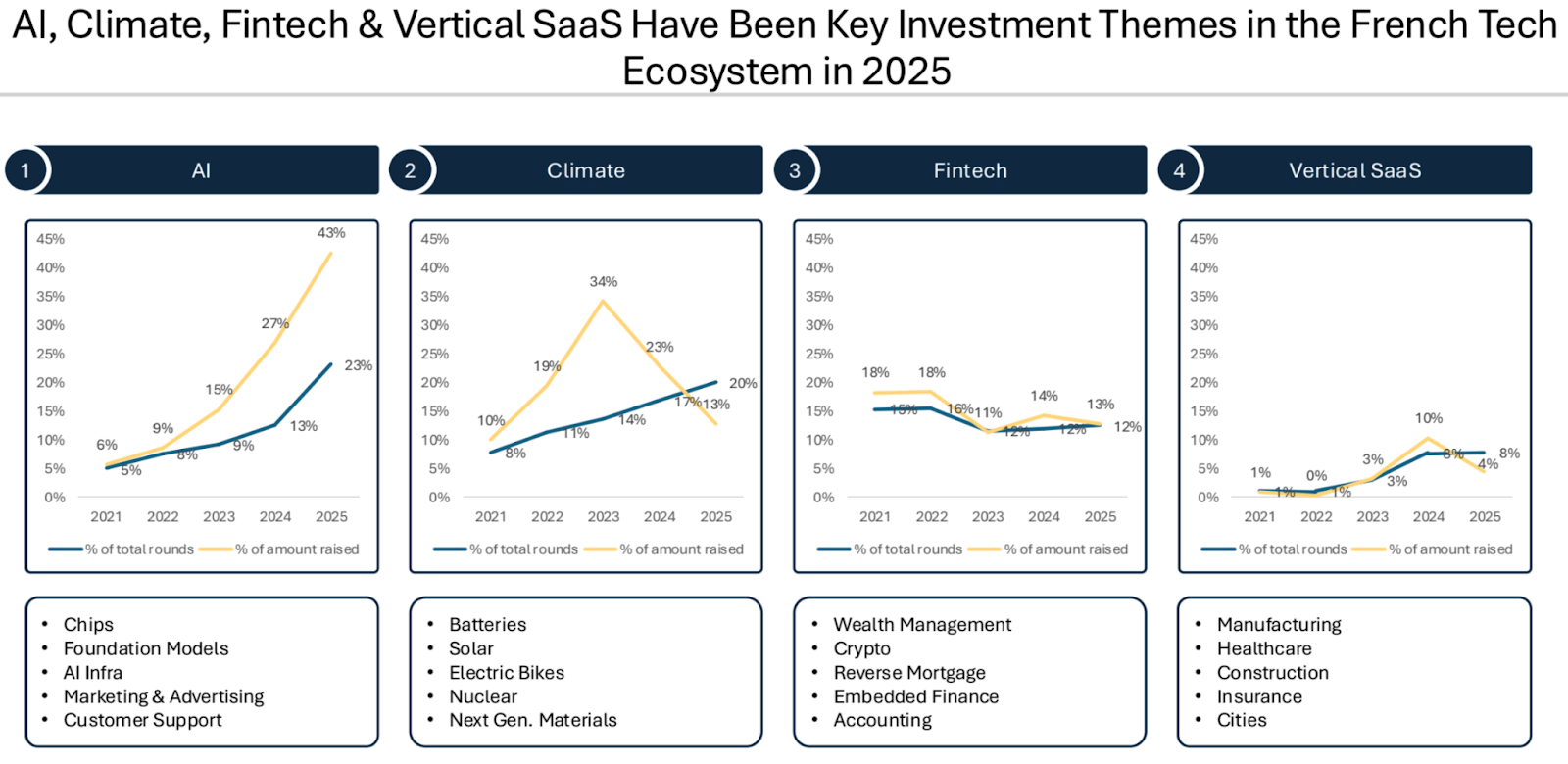

The chart shows a clear concentration of VC investments in a few dominant themes within the French startup ecosystem in 2025. AI stands out, accounting for 23% of total rounds and 43% of capital raised, up sharply from 13% and 27% respectively in 2024. Climate tech remains significant, representing 20% of rounds and 13% of funding, down from a 34% funding peak in 2023. Fintech has stabilized around 12% of both rounds and capital, while Vertical SaaS continues to grow modestly, reaching 8% of rounds and 4% of invested capital, reflecting selective thematic conviction among investors.

But let’s take a closer look at the main news of the last seven days. Capital One acquires Brex for $5.15B, Airwallex expands in South Korea with Paynuri acquisition, and the European Commission finally announces EU-Inc! But also, PayPal acquired Cymbio, NYSE launches a 24/7 tokenized securities platform, Revolut moves into Peru with a full banking license application and integrates Revolut Pay with Google. Lots of movements in the VC ecosystem! Portage assumes control of Point72 Ventures fintech portfolio for $282M, DTCP closes a $500M fund, Ananda Impact Ventures a $73M fifth fund. But also new funds from Vanagon, IQ Capital, Plural, Demium and Fracttal. And finally, some very interesting funding rounds from fintech startups like Sinpex, Magie, CheckSig, Pomelo, Pennylane, Stream, Finst and many others.

But let’s take a closer look:

Rounds

Sequoia Capital breaks its own rule to avoid investments in competitors by backing Anthropic in $25B+ AI round

Sinpex raises €10M Series A to scale AI driven KYB across Europe

Magie raises $5M to bring conversational finance to WhatsApp for businesses

General Atlantic ups its bet on Odoo at a €7B valuation

CheckSig raises €3.5M to scale regulated crypto services across Europe

Pennylane raises $200M to scale AI accounting for Europe’s SMEs

Pomelo raises $55M Series C to build the stablecoin and real time payments layer for LatAm

Stream raises $90M Series D to scale workplace finance and pensions

Cardtonic (The Tonic Technologies LTD) raises $2.1M to launch Pil business spending platform

AssetPlus raises Rs 175 Cr to scale wealthtech platform and product suite

Embankment raises €15M Series A to scale fund tech and expand in Luxembourg

Crunched raises $6M to bring AI native analysis inside Excel

Andreas Klinger raises €15M for Prototype to back Europe’s deep industrial founders

Obside AI raises €500K to democratise AI driven automated trading

Sea adds S$75M to MariBank Singapore as revenue more than doubles

Finst raises €8M Series A to accelerate regulated crypto expansion in Europe

Datarails raises $70M Series C as AI finance agents enter the enterprise

ZBD raises $40M Series C to scale bitcoin payments in gaming

OneDosh raises $3M pre seed to build stablecoin rails for cross border payments

Superstate raises $82.5M Series B to scale tokenized securities infrastructure

VC funds

Portage assumes management of Point72 Ventures’ fintech portfolio via $280M continuation vehicle

DTCP raises €500M fund for “Project Liberty” to scale European defence and resilience tech

Vanagon Ventures closes €20M fund to back Europe’s deeptech at pre-seed

Ananda Impact Ventures secures €73M first close for fifth impact fund

IQ Capital secures £50M commitment for fund V from British Business Bank

Demium rebrands as Mission and launches €35M pre seed fund in Spain

Fracttal raises $35M to scale AI driven asset maintenance globally

News on the market

Revolut moves into Peru with full banking licence application

Monzo Bank launches free in app tax filing tool ahead of UK MTD changes

Revolut Pay integrates with Google AP2 to enable agentic commerce in Europe

NYSE plans 24/7 blockchain platform for tokenized stocks and ETFs

EU–INC: Europe finally moves toward a single startup company regime!

Gokind and Creditsafe partner on real time fraud intelligence in the Nordics

Gusto introduces stablecoin payouts for international contractors

Airwallex expands into Korea with Paynuri acquisition

Checkout.com powers payments for Freenow by Lyft across Europe

COCA crosses $1B valuation as stablecoin banking gains traction

PayPal acquires Cymbio to embed commerce directly inside AI platforms

Capital One acquires Brex for $5.15B in a landmark fintech deal

Italian market

-

And here some useful resources for everyone involved in the ecosystem:

Events you don’t want to miss

FIBE | Berlin - 15th-16th April 2026 (Link here)

Stablecon EMEA | Amsterdam - 19th-20th May (Link here)

You have a cool event you want to mention or to sponsor? Feel free to send me a DM.

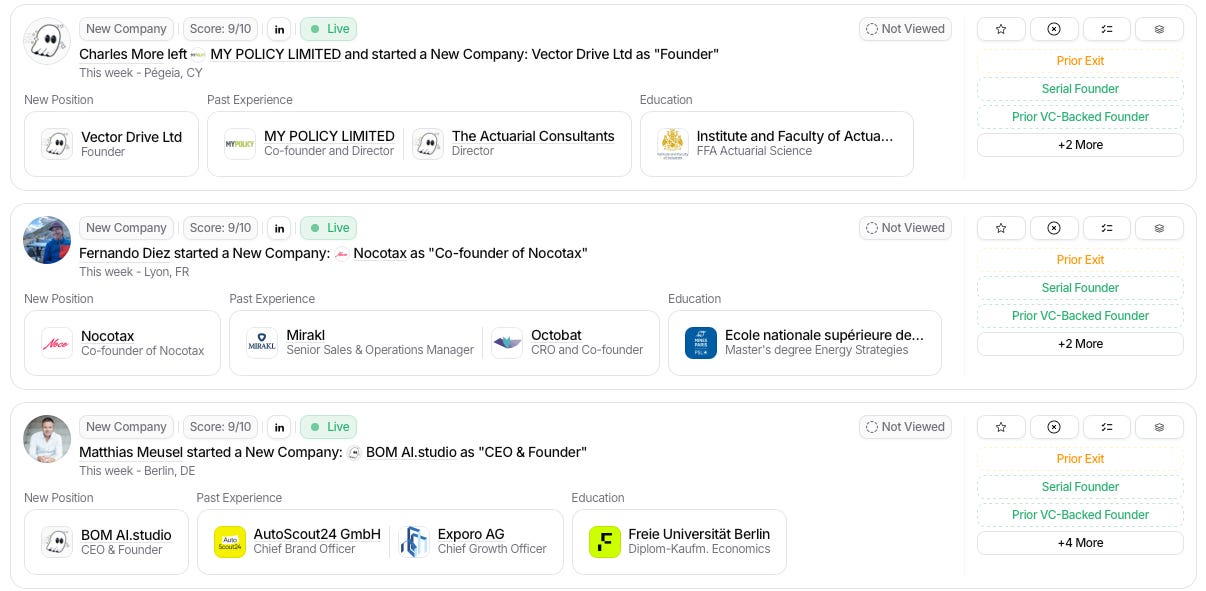

Founders to watch in fintech

I also wanted to start shining a light on the most interesting fintech founders out there, so I thought to start sharing how I look for ideas to invest on. Every week, I will start sharing the most interesting founders in fintech, divided per area. Here an example:

Here you can see the most interesting founders in fintech, in this case in Europe.

I usually use Spectre to scout for new ideas, the team is great and they also give me a free account once they learned I was a fan of the product. So if you wanna take a look at it, you can find it here.

New funds

I recently spoke with Marco Scotti from Raspberry Ventures. Thanks to their Y Combinator Alumni network, they unlock access to the top 10% of YC companies for Angel investors. Co-investing up to $3M across 15 - 25 companies in each YC batch, 4 batches a year, before Demo Day; and before the Silicon Valley VCs come in and take allocations in the best companies.

Their next batch YC W26m is closing February 1st, 2026. You can take a look here if you are interested!

Take also a look at the last edition of the newsletter, Weekly update #115.